In today’s dynamic financial landscape, homeowners often need additional funding beyond their initial home loan. SBI’s Home Top Up Loan program addresses this need by offering existing home loan borrowers access to supplementary funds with competitive interest rates and flexible terms.

State Bank of India (SBI) offers competitive interest rates, starting at 8.30% p.a., for home loan top-ups. Users can also avail of flexible repayments of up to 30 years for their financial needs.

SBI Home Loan Top-Up: Key Features and Highlights

Before diving into the specifics, let’s examine the fundamental aspects that make SBI’s Home Top-Up Loan an attractive option for borrowers seeking additional financing.

| Parameter | Details |

|---|---|

| Interest Range | 8.30% – 11.30% p.a. |

| Maximum Tenure | Up to 30 years |

| Processing Fee | 0.35% of loan amount |

| Minimum Processing Fee | 0.35% of the loan amount |

| Maximum Processing Fee | ₹10,000 (plus GST) |

| Prepayment Charges | 0.35% of the loan amount |

Source: SBI Home Loan Official Website

SBI Home Top-Up Loan Interest Rates 2025

| SBI Top-Up Loan Scheme | Interest Rate (p.a.) |

|---|---|

| SBI Top-Up Home Loan | 8.30% – 10.80% |

| SBI Top-Up Home Loan (OD) | 8.50% – 9.45% |

Check the official interest rates for all SBI home loan products

SBI Home Top-Up Loan Eligibility Criteria

SBI has established comprehensive eligibility parameters to ensure responsible lending while maintaining accessibility. Here’s a detailed breakdown:

| Criterion | Requirement |

|---|---|

| Age | Minimum: 18 years, Maximum: 70 years |

| Nationality | Indian Residents and NRIs |

| Income | Regular source with documented proof |

| Credit Score | Preferably above 750 |

| Existing Loan | A regular source with documented proof |

Source of Data: Check out the official eligibility criteria for SBI Home Loan Top-Ups.

To qualify for an SBI Home Top-Up Loan, applicants must meet the following criteria:

- Must be an existing SBI home loan customer.

- A good repayment track record with timely EMI payments.

- Stable income source (salaried, self-employed, or business owner)

- Sufficient income to cover the increased EMI amount

- The property should have appreciated in value.

- The applicant must be of legal age (at least 18 years) and meet the bank’s creditworthiness standards.

SBI Home Loan Top-Up Processing Fees and Charges

| Loan Type | Processing Fee |

|---|---|

| Home Top-Up Loan | 0.35% of the loan amount plus applicable GST Minimum: ₹2,000 + GST Maximum: ₹10,000 + GST |

SBI Home Top-Up Loan Documents Required

The documentation process for an SBI Home Top-Up Loan is straightforward. Generally, the following documents are required:

| Document Type | Purpose | Acceptable Forms |

|---|---|---|

| Identity Proof | Verification of identity | PAN Card, Passport, Driving License |

| Address Proof | Current residence verification | Utility Bills, Passport, Voter ID |

| Income Proof | Financial capability assessment | Bank Statements, Salary Slips |

| Property Documents | Collateral verification | Original property papers, Tax receipts |

Additional Category-Specific Requirements

For Salaried Individuals:

- Recent salary statements (last 3 months)

- Employment contract or certification

- Form 16 for the last two fiscal years

- Professional qualification certificates (if applicable)

For Self-Employed Professionals:

- Business registration documents

- GST returns (if applicable)

- Profit and loss statements

- Business continuity proof

Also Read: SBI Home Loan Customer Care Contact Details

How to Apply to SBI Home Loan Top-Up?

Follow these steps to apply for an SBI Home Loan Top-Up:

- Eligibility Check: Ensure you meet SBI’s eligibility criteria for a home top-up loan.

- Gather Documents: Prepare the necessary documents such as identity proof, address proof, income proof, and property documents.

- Submit Application: Fill out the application form and submit it along with the required documents to SBI, either online or at a branch.

- Processing Fee: Pay the processing fee, if applicable.

- Verification: SBI will verify your documents and assess your eligibility based on your existing home loan and repayment history.

- Approval: Once the verification is complete, SBI will review your application and, if approved, will sanction the loan.

- Disbursement: After approval, the loan amount will be disbursed to your account.

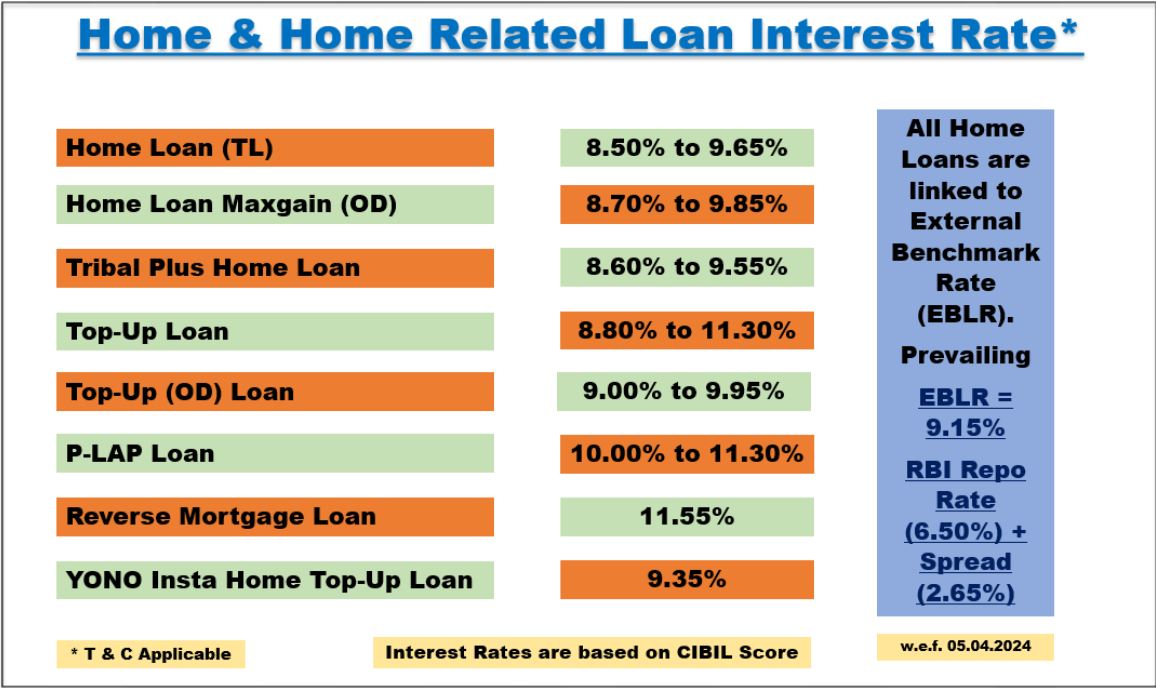

SBI Home Loan: Other Products

| Home Loan Type | Home Loan Interest Rates |

|---|---|

| SBI Regular Home Loan | 8.50% p.a. – 9.65% p.a. |

| SBI Maxgain (Overdraft) | 8.25% p.a. – 9.15% p.a. |

| SBI Tribal Plus Home Loan | 8.60% p.a. – 9.55% p.a. |

| SBI Home Loan Top Up | 8.30% p.a. – 10.80% p.a. |

| SBI Home Loan Top Up (OD) | 8.50% p.a. – 9.45% p.a. |

| SBI Loan Against Property | 9.50% p.a. – 10.80% p.a. |

| SBI Reverse Mortgage Loan | 11.05% p.a. onwards |

| SBI YONO Insta Home Loan Top Up | 8.85% p.a. onwards |

Compare Top Banks Home Loan Top-Up Interest Rates

| Bank | Interest Rate (p.a.) |

|---|---|

| State Bank of India | 8.00% onwards |

| HDFC Bank | 8.70% – 9.55% |

| ICICI Bank | 8.75% onwards |

| Axis Bank | 8.75% – 12.80% |

| Kotak Mahindra Bank | 8.65% onwards |

| Punjab National Bank | 8.50% onwards |

| Bank of Baroda | 8.40% onwards |

Get the Best SBI Home Loan Offers with Credit Dharma

Credit Dharma is your trusted partner for securing the best SBI Home Loan offers, with over ₹500 Cr+ loans handled and partnerships with 20+ leading banks. We provide exclusive access to the lowest interest rates and a seamless, digital process with fast approvals in just 1-2 weeks, backed by lifetime support from our home loan experts.

Why choose Credit Dharma? We provide:

- Lowest Interest Rates: Save more with every EMI.

- Maximum Funding: Get up to 100% funding for your dream home.

- Simple & Digital Process: No tedious paperwork or branch visits.

- Expert Guidance: Lifetime support from our team of specialists.

Compare, choose, and secure the best SBI Home Loan offer with Credit Dharma — your home loan journey starts here!

Before applying, carefully consider your financial situation and repayment capacity to ensure that the top-up loan aligns with your long-term financial goals. If you need any guidance or help shaping the plan for your home loan journey, reach out to Credit Dharma. We offer free consultation calls to help you navigate your home loan journey.

Conclusion

The SBI Home Top-Up Loan is a valuable financial product for existing home loan customers, offering flexibility and convenience. With competitive interest rates, no prepayment charges, and the ability to use the funds for various personal needs, it stands out as an attractive option for those looking to meet their financial requirements without the complexities of a new loan application.

Frequently Asked Questions

An SBI Home Loan Top-Up is an additional loan amount that existing SBI home loan borrowers can avail over and above their current home loan. This facility allows borrowers to access extra funds for personal needs such as home renovation, education, or medical expenses.

Existing SBI home loan customers with a satisfactory repayment track record are eligible for a top-up loan. Both resident Indians and NRIs can apply. The minimum age requirement is 18 years, and the maximum age is 70 years.

The maximum loan amount depends on various factors, including the value of the existing home loan and the bank’s assessment of the borrower’s repayment capacity. For the Insta Home Top-Up Loan, the maximum limit is 8% of the home loan amount or ₹8 lakh, whichever is lower.

Interest rates for SBI Home Loan Top-Up range from 8.80% to 11.30% per annum, depending on the applicant’s credit score and other factors

The repayment tenure can extend up to 30 years, subject to the condition that it does not exceed the residual tenure of the existing home loan.

Yes, a processing fee of 0.35% of the loan amount is applicable, with a minimum of ₹2,000 and a maximum of ₹10,000, plus applicable GST.

The top-up loan can be used for various personal needs, such as home renovation, education, or medical expenses. However, it should not be used for speculative purposes.

Eligible customers can apply for a top-up loan by visiting their nearest SBI branch or through the YONO app for the Insta Home Top-Up Loan.

The documentation process is similar to that of the original home loan and may include identity proof, address proof, income proof, and existing home loan details.

No, there are no prepayment or pre-closure penalties for SBI Home Loan Top-Up, allowing borrowers to repay the loan earlier without additional costs.

HDFC Home Loan

HDFC Home Loan SBI Home Loan

SBI Home Loan

{kind=link}