HDFC Bank, like most lenders, uses the borrower’s credit score to assess risk. While many lenders don’t publicly disclose exact cutoffs, a score of 750+ is generally considered safe.

Curious where you stand? Are you eligible for a home loan from HDFC Bank? Let’s explore the benchmarks and how to polish your credit profile before applying.

You deserve a better home loan interest rate. Check your CIBIL Score Today!

Minimum CIBIL Score Requirements for HDFC Bank Home Loan

A minimum CIBIL score of around 750 is usually preferred to easily secure a home loan at attractive terms. Higher scores improve your chances of getting better rates. Here’s what different score ranges indicate:

| CIBIL Score Range | Meaning | Tentative Interest Rates |

|---|---|---|

| 800 – 900 | Excellent score; indicates timely payments with no defaults, making loan approval easy and interest rates favorable. | 8.15%* p. a. Onwards |

| 750 – 800 | Very good; helps in negotiating lower interest rates due to a strong credit history. | 8.15%* p.a. Onwards |

| 625 – 750 | Average score; acceptable but may attract slightly higher interest rates and stringent terms. | 8.30%* p.a. Onwards |

| 300 – 625 | Poor score; frequent missed payments and defaults. Loan approvals are difficult without improving this score. | 11%* p.a. Onwards |

How to Check Your CIBIL Score Before Applying for HDFC BankHome Loan?

- Navigate to the official website of CIBIL.

- Click on Get Your FREE CIBIL Score

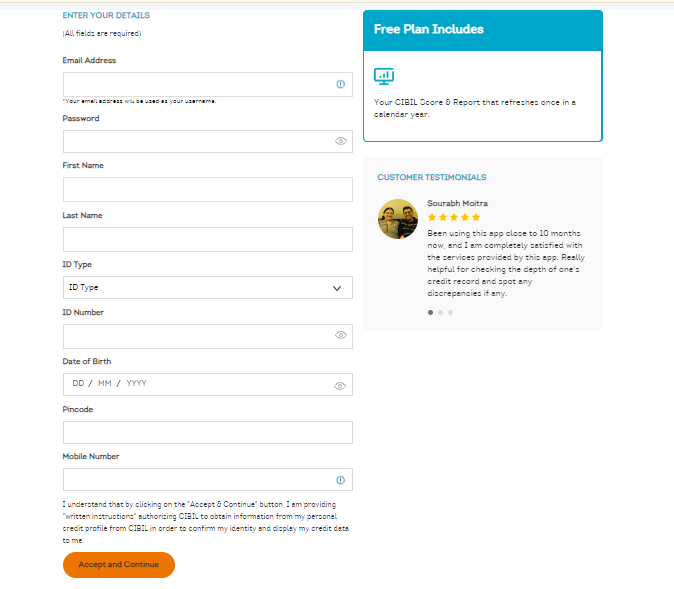

- Enter your basic details, including, Email Address, Name, ID Proof (PAN CARD), Date of Birth, and Mobile Number. Click on Submit.

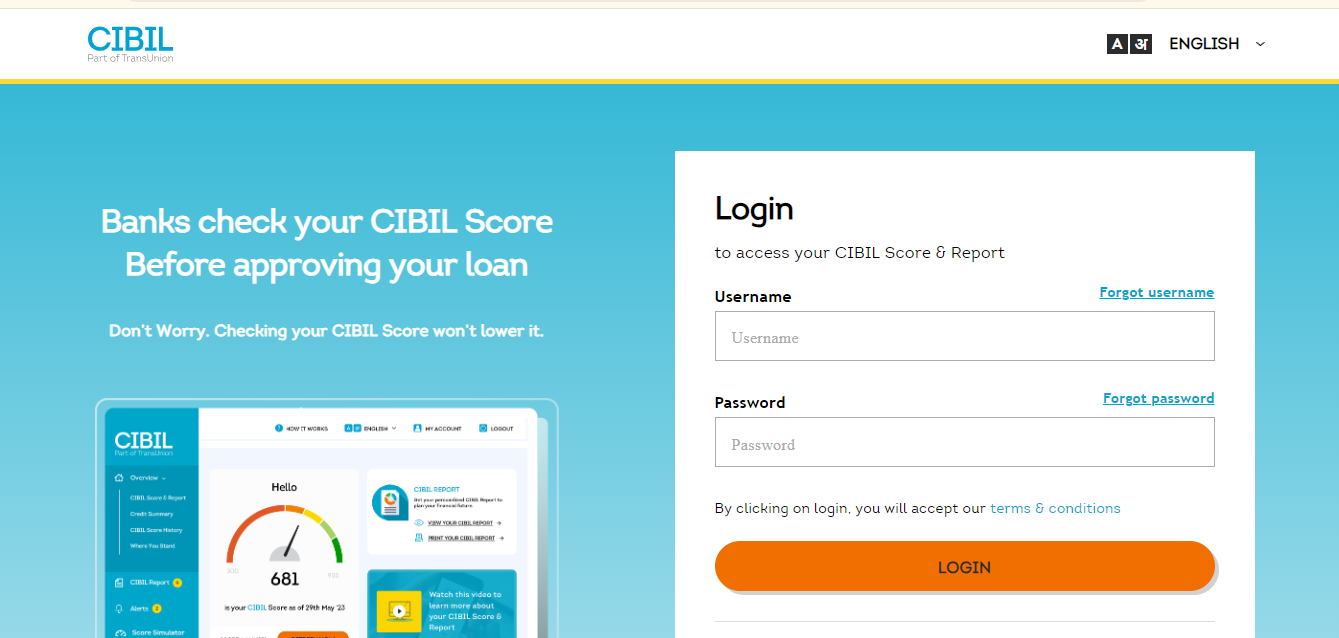

- Once you have created your account, login using your Email ID and Password.

- An OTP will be sent to your registered mobile number, enter the OTP and proceed.

- Your CIBIL Score will be displayed on the screen.

Read More: CIBIL Score Check Free Online by PAN Number

How to Get CIBIL Score Report Offline?

- Download the application form from the CIBIL website. Free CIBIL Score and Report.

- Fill out the form accurately with all your required details.

- You’ll need to pay a fee to acquire your CIBIL report. The amount varies depending on whether you just want the score or the detailed report.

- For both the CIBIL score and the complete report, the fee is Rs. 550.

- To receive only the CIBIL report, the fee is Rs. 164.

- Make a demand draft (DD) payable to “TransUnion CIBIL Limited” for the chosen amount.

- Mail the completed application form along with the DD to the following address:

TransUnion CIBIL Limited

One India Bulls Centre, Tower 2A, 19th Floor

Senapati Bapat Marg, Elphinstone Road

Mumbai – 400013

Download CIBIL Score Application Form here

Key Benefits of a Good CIBIL Score for HDFC Bank Home Loans

- A high CIBIL score speeds up the HDFC Bank home loan approval process.

- It helps you secure lower interest rates on your home loan.

- A good score increases the maximum loan amount you can get.

- It allows you to choose from more flexible EMI and repayment options.

- You gain better negotiating power on interest rates and fees.

- It leads to faster disbursal of your sanctioned home loan.

- You become eligible for top-up loans with minimal checks.

- Lenders trust your profile more, reducing the chances of rejection.

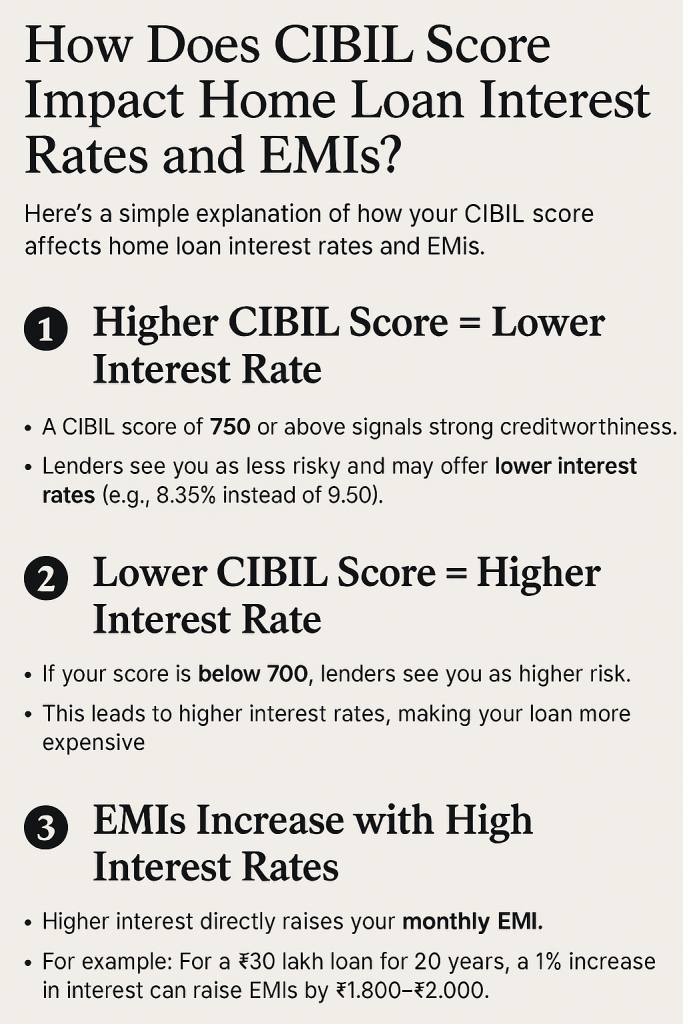

How Does CIBIL Score Impact Home Loan Interest Rates and EMIs?

Here’s a simple explanation of how your CIBIL score affects home loan interest rates and EMIs:

1. Higher CIBIL Score = Lower Interest Rate

- A CIBIL score of 750 or above signals strong creditworthiness.

- Lenders are more confident and may offer lower interest rates (e.g., 8.35% instead of 9.50%).

2. Lower CIBIL Score = Higher Interest Rate

- If your score is below 700, lenders see you as a higher risk.

- This leads to higher interest rates, making your loan more expensive.

3. EMIs Increase with High Interest Rates

- Higher interest directly raises your monthly EMI.

- Example: For a ₹30 lakh loan for 20 years, a 1% increase in interest can raise EMIs by ₹1,800–₹2,000.

How Does Adding a Co-Applicant Improve Your CIBIL Score Eligibility?

Adding a co-applicant to your loan application can significantly improve your CIBIL score eligibility. When you apply with a co-applicant, the lender considers both incomes, which boosts your overall repayment capacity. This makes it easier to qualify for higher loan amounts.

If your co-applicant has a strong CIBIL score, it strengthens your application and increases the chances of approval, especially if your own score is low.

Lenders also view joint applications as less risky, which can lead to better interest rates. Over time, if you repay the loan on time, it helps improve both your and your co-applicant’s credit scores.

This strategy is especially useful for those with a limited credit history or lower income, as it makes the application more stable and creditworthy.

How to Improve Your CIBIL Score in 3 Months?

- Pay all bills/EMIs on time to maintain a flawless payment history.

- Reduce credit card utilization below 30% of your total limit.

- Clear high-interest debts first (e.g., credit cards, personal loans).

- Avoid applying for new credit to prevent hard inquiries.

- Check and dispute errors in your CIBIL report immediately.

- Maintain a balanced credit mix (secured loans like home loans, unsecured loans like credit cards).

- Don’t close old credit accounts to preserve credit history length.

- Use a credit monitoring tool to track progress and alerts.

- Pay credit card bills in full instead of minimum payments.

- Request a credit limit increase (if possible) to lower the utilization ratio.

Alternative Financing Options for Borrowers with Low CIBIL Scores

- Non-Banking Financial Companies (NBFCs): Offer home loans to low CIBIL scorers with higher interest rates or collateral requirements.

- Co-Signer/Co-Borrower: Add a family member with a strong credit profile to strengthen the application.

- Secured Loans Against Assets: Use gold, fixed deposits, or property as collateral for loans (e.g., gold loans, loan against FD).

- Government Housing Schemes: Explore PMAY (Pradhan Mantri Awas Yojana) subsidies or affordable housing schemes with relaxed eligibility.

- Loan Against Property (LAP): Use an existing property as collateral for a secured loan (even with low CIBIL).

Conclusion

Securing a home loan with HDFC Bank significantly depends on your CIBIL score. By understanding and proactively managing your creditworthiness, you enhance your chances of approval and favorable loan terms.

Even if your current credit score is low, Credit Dharma can help you get a home loan by leveraging their expertise and tailored solutions to work around credit challenges.

Frequently Asked Questions

You may face higher interest rates, stricter eligibility criteria, or potential loan rejection due to higher perceived credit risk.

Pay your bills on time, reduce existing debt, avoid multiple loan applications, and correct any inaccuracies in your credit report.

Yes. Lenders also consider your income stability, employment history, existing financial obligations, and the property’s value.

Checking once every few months (at least quarterly) is recommended to monitor changes and catch errors quickly.

Holding multiple loans can increase your credit utilization, potentially lowering your score if repayment capacity seems stretched.

HDFC Home Loan

HDFC Home Loan SBI Home Loan

SBI Home Loan