A debt consolidation loan is a single new loan you take out to pay off several existing debts (like credit-card balances, home loans, or other personal loans). After that, instead of making many separate payments each month, you make just one payment to the new lender.

Indian Consumer – Debt Landscape

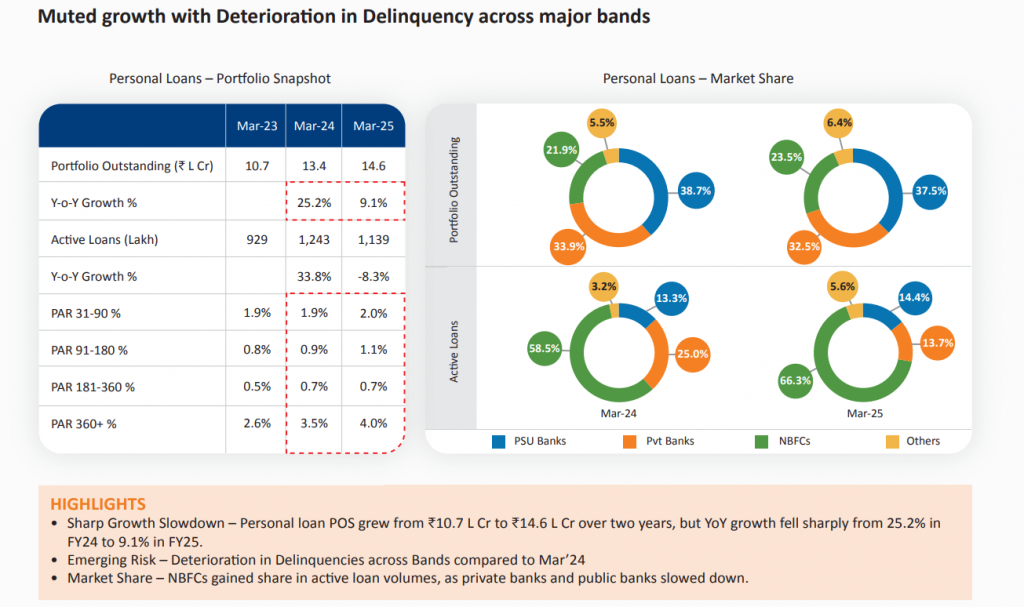

Indian households have steadily embraced unsecured credit. Personal-loan growth averaged 25.2% a year between FY22 and FY24, although it moderated to 9.1% by January 2025 after regulatory tightening. Private-sector banks now hold more than half of all gross NPAs in unsecured retail loans, underscoring the need for prudent borrowing. Against this backdrop, many borrowers juggle credit-card dues, consumer-durable EMIs and small personal loans—prime candidates for consolidation.

Types of Debt Consolidation Loans

If juggling several loan and credit-card bills each month feels messy and expensive, you’re not alone. Depending on your credit profile, how quickly you can repay, and whether you own a home, you might choose:

1. Personal Loan

A personal loan is money you borrow from a bank, credit-union, or online lender without pledging any property. You use the lump sum to wipe out several smaller balances, then repay the new loan in set monthly installments.

Why people like it

- No house, car, or valuables required as security

- Fixed interest rate and a clear payoff schedule

- Funds typically arrive within days

Works best for: Clearing high-interest credit-card bills or a handful of small loans you want off your plate quickly.

2. Balance-Transfer Credit Card

Some credit cards let you shift existing card balances onto a fresh card that charges little to no interest for an introductory period—often 6 to 18 months. During that window, every rupee you pay goes toward knocking down the principal instead of interest.

Why people like it

- 0% or very low interest for a limited time

- One card statement instead of many

- No new loan paperwork

Works best for: Short-term debt you’re confident you can erase before the promo rate expires.

3. Home-Equity Loan

If you own a home and have built up equity (the home’s value minus what you still owe), you can borrow against that equity and use the cash to pay off other debts. Because the loan is secured by your property, interest rates are usually lower than with unsecured loans.

Why people like it

- Typically the lowest rates of the three options

- Longer repayment periods mean smaller monthly payments

- Interest may be tax-deductible in some regions

Works best for: Large debt totals, especially if you’re comfortable using your home as collateral and plan to stay there for a while.

4. Unsecured Business Loan

An unsecured business loan is money borrowed for business purposes without requiring collateral or security. These loans are approved based on creditworthiness, business financials, and repayment capacity rather than asset pledges.

Why people like it:

- No collateral required: Eliminates risk of losing valuable business assets

- Faster processing: Quick approval and disbursal, often within 24-48 hours

- Flexible use of funds: Can be used for debt consolidation, working capital, equipment purchases, or expansion

Works best for: Businesses looking to consolidate multiple high-interest debts without pledging assets, especially suitable for MSMEs and startups with limited collateral

5. Short-Term Working Capital Loan

A short-term working capital loan is designed to finance day-to-day business operations and cover immediate cash flow needs. These loans help businesses manage temporary financial gaps and operational expenses.

Why people like it:

- Short tenure: Typically ranges from 3 months to 1 year, making it ideal for immediate needs

- Quick disbursal: Fast processing and approval, often same-day funding available

- Unsecured options: Many working capital loans don’t require collateral

- Flexible repayment: Aligned with business cash flow cycles

- Revolving credit facility: Some offer the ability to withdraw, repay, and borrow again as needed

Works best for: Businesses experiencing seasonal fluctuations, inventory purchases, payroll management, covering operational expenses during cash flow gaps, or managing temporary working capital shortages.

Suggested Read: Best Consolidation Loans in August 2025 | CNBC

Debt Consolidation Loan Interest Rates 2025

Interest rates on debt-consolidation loans are hovering well below last year’s highs, but they still vary widely by lender and credit score

| Bank/ NBFCs | Interest Rates |

|---|---|

| HDFC Bank | 11.25% p.a. onwards |

| IDFC First Bank | 9.99% p.a. onwards |

| Tata Capital | 11.50% p.a. onwards |

| Bajaj Finance | 10.00% p.a. onwards |

| Axis Bank | 16.00% p.a. onwards |

| SBI | 10.30% p.a. onwards |

How Does Debt Consolidation Loan Work?

Rolling multiple high-interest debts into one lower-cost personal loan can reduce monthly cashoutgo by one-quarter and bring a clear debt-free timeline—but only when the new loan’s proceeds are used immediately to extinguish the old balances and the borrower avoids re-borrowing.

Borrower Profile & Pre-Consolidation Position

Rajesh (salaried, CIBIL 760) was juggling three unsecured obligations:

| Original Lender | Outstanding | Annual Rate | Monthly Due Date | EMI / Min-Pay |

|---|---|---|---|---|

| Credit-card A | ₹1,00,000 | 36% (3% pm) | 5th | ₹3,500 (min-pay ∼3.5%) |

| Consumer loan (NBFC) | ₹80,000 | 16% | 15th | ₹2,800 |

| Credit-card B | ₹50,000 | 18% (1.5% pm on EMI-converted spend) | 25th | ₹2,000 |

| TOTAL | ₹2,30,000 | — | three dates | ₹8,300 |

Three separate due dates increased the risk of missed payments and penalty interest.

Consolidation Transaction

Rajesh applied for an IDFC FIRST FIRSTmoney personal loan structured specifically for debt consolidation:

- Loan amount sanctioned: ₹2,30,000 (equal to aggregate dues)

- Tenure: 48 months

- Fixed interest rate: 9.99% p.a. (processing fee 2%)

- Disbursal instructions: lender paid both credit-card issuers directly and credited the NBFC loan closure account, collecting No-Dues letters.

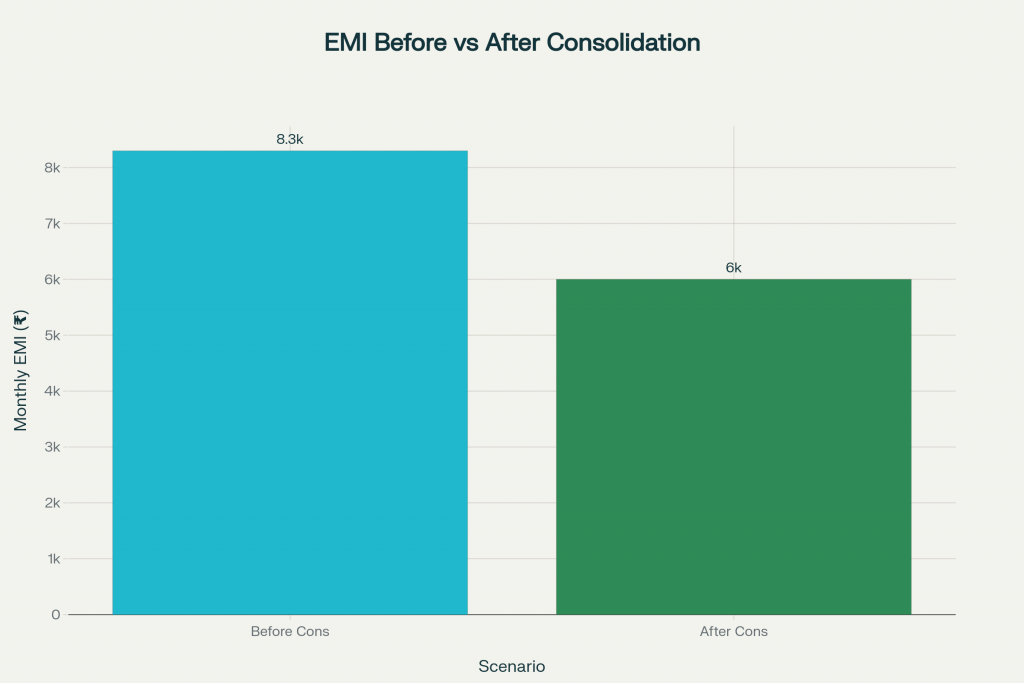

Post-Consolidation Cash-Flow

New single EMI ≈ ₹6,000 (confirmed in the case study table) — a 28% drop from the previous ₹8,300. The lower rate and longer tenure drive the saving.

What Really Happened to the Old Debts?

- Credit-cards: Limits stayed open but utilisation fell to 0%; Rajesh set alerts to avoid fresh spends until the consolidation loan is repaid.

- NBFC loan: Account closed, bureau updated within 7 days under RBI fortnightly reporting rule.

- Credit score impact: Small inquiry-led dip (~5 points) recovered within two months as utilisation plunged and payment history stayed perfect

Interest-Cost Math

Had Rajesh kept the status quo:

- Credit-cards at 3% pm interest on revolving ₹1.5 L would add ≈ ₹4,500 interest in the first month alone; minimum-due cycling projected total interest near ₹2 lakh over four years.

Under the consolidation loan:

- Total interest over 48 months ≈ ₹48,500 (₹6,000 × 48 – ₹2.30 L principal) — almost 75% less than continuing to revolve the cards.

Who Qualifies for a Debt Consolidation Loan?

- Credit score: 670 + unlocks the best rates; below 580 usually needs collateral or a co-signer.

- Debt-to-income ratio (DTI): Keep total monthly debt under 40 % of income for unsecured loans.

- Stable income: Proof of steady pay (or two years’ business returns if self-employed) reassures lenders.

- Clean recent history: No 90-day lates, defaults, or active collections in the last 12 months.

- Collateral (optional): Home equity or a vehicle title can offset weaker credit for secured consolidation.

Suggested Read: Debt Consolidation vs. Credit Card Refinancing

Who Should Consider Debt Consolidation?

At a glance: Consolidate when one lower-cost loan can replace multiple high-interest EMIs, reduce your monthly outgo, and cut total interest, without tempting you back into fresh debt.

Who Typically Benefits

- Managing three or more EMIs with scattered due dates.

- Paying very high interest (e.g., credit cards at ~40%+), yet eligible for ~11–13% consolidation rates.

- Credit score around 650 or higher (helps qualify for advertised rates).

- Stable, predictable income (salary or steady business inflows).

- Disciplined with spending after cards/loans are cleared.

When the Timing Is Right

- Your combined EMIs are high enough that one consolidation loan would meaningfully reduce the monthly outgo.

- The projected monthly saving remains clearly significant even after fees and charges.

- Income and cash flows appear stable for the next several months.

- You have a straightforward plan to avoid re-borrowing on cleared cards or limits (close/downgrade or reduce limits).

When to Proceed with Caution

- Total debt is over 50% of your annual income.

- You’re focused only on a lower EMI but total interest would rise.

- Spending triggers (lifestyle/impulse purchases) are not addressed.

What Credit Score Do You Need for Debt Consolidation?

| Credit Score Range | Rating | What It Means |

|---|---|---|

| 750+ | Excellent | Lowest APRs, highest credit limits, easy approval |

| 700–749 | Good | Competitive rates, approval from most mainstream lenders |

| 650–699 | Fair | Likely approval, but with higher interest or smaller loan amounts |

| 580–649 | Poor | May need co-signer/collateral; high interest rates |

| Below 580 | Very Poor | Unlikely approval; consider nonprofit credit counseling instead of new loans |

Documents Required for a Debt Consolidation Loan

Indian lenders treat most consolidation loans as standard unsecured personal loans, so the documentary checklist largely mirrors RBI-mandated KYC and income proofs:

| Document Category | Accepted Documents |

|---|---|

| 1. Identity & Address Proof (OVD) | Aadhaar (with full number) Passport Voter ID Driving Licence NREGA Job Card NPR Letter (One OVD with name & address suffices if both addresses match) |

| 2. PAN & Photograph | PAN Card (mandatory for loans > ₹50,000) Recent Passport-size Photograph |

| 3. Income Evidence | Last 2–3 Salary Slips 3–6 Months’ Salary-Credit Bank Statements Form 16 / ITR (last 2 years) |

| 4. Employment Verification | Employee ID Card or HR Letter (salaried) GST Returns Business Registration Shop Licence (self-employed) |

| 5. Loan-Specific Paperwork | Filled Loan Application Form e-Mandate/NACH Setup Processing Fee Acknowledgement Property Papers Valuation Report Insurance (for secured loans) |

Pros and Cons of Debt Consolidation Loan

Like any financial decision, debt consolidation comes with trade-offs. Here’s a quick look at the key pros and cons to help you decide if it’s the right solution for your situation.

Pros of a Debt Consolidation Loan

- Single monthly payment: One due date makes budgeting and autopay simple.

- Potentially lower interest: If your new APR beats the average of your current debts, you save money.

- Fixed payoff date: Installment loans have an end point, giving you a clear “debt-free” timeline.

- Possible credit-score boost: Paying off high-utilization credit cards can raise your score after a few on-time payments.

- Reduced stress: Fewer statements and notifications mean less mental clutter.

Cons of a Debt Consolidation Loan

- Up-front costs: Origination or balance-transfer fees can eat into savings.

- Longer repayment term risk: Stretching the loan for a lower EMI may increase total interest paid.

- Credit requirements: The best rates usually demand good to excellent credit; weaker profiles see higher APRs or refusals.

- Temptation to re-spend: Running up balances on newly cleared cards can land you in deeper debt.

- Asset risk for secured loans: If you use home equity or another collateral, missed payments could cost you that asset.

Impact of Debt Consolidation on Your Credit Score

Debt consolidation can be a smart financial move, but how does it impact your credit score? The answer depends on how you manage the process across different timeframes.

| Timeline | Impact on Credit Score |

|---|---|

| Immediate Effects | Hard Inquiry Dip: Each loan application causes a bureau check, typically reducing your score by 5–10 points temporarily. Average Account Age Falls: Opening a new loan slightly lowers your credit history length. |

| Medium-Term Shifts | Utilisation Ratio Improves: Paying off credit card balances lowers your credit usage, boosting scores. Healthier Credit Mix: Adding an instalment loan diversifies your credit profile. |

| Long-Term Outcomes | Improved Repayment History: Regular EMI payments build a positive credit record, the most important factor in your score. Net gains usually appear within 12–18 months. |

| Potential Pitfalls | – Closing old credit cards can reduce your total available credit and hurt utilisation ratio. – Running up balances again on cleared cards signals financial instability. – Missing EMIs on the new loan harms your credit just like any other default. |

Consolidation without behaviour change is just a reshuffle.

When I work with clients who are juggling multiple high-interest debts, consolidation can reduce their overall interest burden by 5-10 percentage points while providing the psychological benefit of having one clear target to focus on.

However, success depends entirely on addressing the spending behaviours that created the debt in the first place.

– Sanjay Bharti, Loan Expert | Credit Dharma

Debt Consolidation vs. Debt Settlement

Conclusion

Credit Dharma helps you replace multiple loans and card dues with a single, lower‑cost EMI. With ₹500 Cr+ facilitated and 20+ bank/NBFC partnerships, we secure competitive rates and a fully digital journey—so high‑cost balances get closed in 7–14 days, backed by lifetime support from our consolidation specialists.

Why choose Credit Dharma for Debt Consolidation?

- Market‑best rates: We shop 20+ lenders to beat high credit‑card and personal‑loan interest.

- One EMI, less stress: Merge all eligible dues into a single EMI for predictable cash flow.

- Right size, right tenure: Cover 100% of eligible outstanding with flexible tenures and optional top‑up.

- End‑to‑end & digital: e‑KYC, e‑sign, and we coordinate closures/balance transfers with your existing lenders.

- Fast turnaround: From application to disbursal in 7–14 days.

- Expert guidance, for life: A dedicated specialist supports you before, during, and long after disbursal.

Frequently Asked Questions

Temporarily, yes—a loan application results in a “hard inquiry” and a slight score dip. But as you repay your consolidation loan on time and your credit utilization drops (because old debts get paid off), your score can actually rise above its original level over six to twelve months, assuming you don’t miss payments or rack up new debts.

0% balance-transfer credit cards (pay off card debt within 3–6 months at zero/low interest)

Gold loans or loan against property (if you have assets)

Restructuring existing loans with your lender

Self-payoff strategies like the snowball (smallest balance first) or avalanche (highest rate first)

As a last resort, individual insolvency process under India’s Bankruptcy Code

Yes, you can, but it’s best to clear all high-interest debts in one go so you have only one payment and avoid managing multiple liabilities.

Yes, here’s what to watch out for:

Processing/insurance fees can add 2–4% to your loan amount.

Extending your loan tenure lowers EMI but may mean more total interest paid over the loan’s life.

Secured loans (like a loan against property) put your home at risk if you default.

If you re-use and max out cleared credit cards, your debt could return worse than before.

You don’t have to, but it’s wise to avoid using them until you significantly pay down your consolidation loan. Keeping old cards open (with zero or low utilization) is actually good for your credit score.

HDFC Home Loan

HDFC Home Loan SBI Home Loan

SBI Home Loan