Managing a business in India comes with the constant challenge of maintaining adequate cash to cover daily operations. This is where working capital loans become vital—offering financial lifelines to ensure uninterrupted business activities, handle unexpected expenses, and ride out seasonal cash flow fluctuations.

What is a Working Capital Loan?

A working capital loan is a short-term financing solution designed to cover operational needs such as salaries, inventory, rent, utility payments, and vendor bills. Unlike term loans that fund business expansion or fixed asset acquisition, working capital loans address immediate financial requirements and bridge liquidity gaps, especially for MSMEs and growing businesses.

Working Capital Loan Interest Rates in India (2025)

Interest rates are competitive and vary based on lender, applicant profile, loan amount, and tenor. Here is a snapshot of current business/working capital loan interest rates as of July 2025:

| Loan Type | Interest Rate (p.a.) |

|---|---|

| Overdraft | 8.50% – 15% |

| Cash Credit | 8.50% – 15% |

| Term Loan | 8.50% – 15% |

Note: Actual rates depend on credit assessment, collateral, business profile, and market conditions. Always compare lenders before applying.

Suggested Read: Working Capital vs Fixed Capital

Eligibility Criteria for Working Capital Loans

While every lender may have slight variations, here are the most common eligibility factors:

| Criteria | Details |

|---|---|

| Age | 21 to 65 years (at loan maturity) |

| Business Type | Individuals, partnerships, private/public companies actively engaged in business |

| Turnover & Profit | Minimum business turnover (e.g., above ₹7.5 crore for HDFC Bank) and profitable records |

| Business Vintage | Typically, at least 2-3 years of profitable business operations at the current location |

| Credit Score | 685-700+ is usually required |

| Financial Stability | Proof of profitability, healthy balance sheets, and IT returns |

Eligibility may differ for public schemes like Mudra loans or for priority sector lending by public sector banks.

Check Out: Working Capital Management to Accelerate Growth

Top Working Capital Loan Providers in India

- Banks: HDFC Bank, Axis Bank, ICICI Bank, Kotak Mahindra Bank, SBI, IDFC First Bank

- NBFCs: LendingKart, Tata Capital, Flexiloans, UGRO Capital

- Public Institutions: SIDBI (Small Industries Development Bank of India)

- Government Schemes: Pradhan Mantri Mudra Yojana, CGTMSE (for MSMEs)

Check Out: Working Capital Cycle

Types of Working Capital Loans in India

Source: Navigating Eligibility – Working Capital Loans Explained

Documents Required for Working Capital Loan in India

While documentation requirements can vary slightly among lenders, most banks and NBFCs ask for the following:

| Document Type | Examples/Details |

|---|---|

| KYC (ID & Address Proof) | PAN, Aadhaar, Passport, Driving License, Recent Utility Bill |

| Business Registration | GST, Incorporation Cert., Trade License, Partnership Deed, Udyam/ MSME |

| Financials | Audited P&L, Balance Sheet (2–3 yrs), Tax Returns (2–3 yrs), GST |

| Bank Statements | Last 6–12 months |

| Ownership/Continuity | Property Ownership/Lease Proof, Sales Tax Return, Registration Cert. |

| Collateral (if required) | Property Deeds, Asset Docs |

| Other | Photographs, MOA/AOA, Board Res., Loan Letters, Invoices |

Tip: Having all documents organized and up-to-date increases your chances of quick approval and smooth disbursal of working capital loans.

Check Out: What is a Working Capital Loan?

Application Process for Working Capital Loans

Efficiently secure the funds your business needs by following these simple steps for applying for a working capital loan in India.

- Assess Needs:

Determine your cash flow gap and the right loan product.

- Choose a Lender:

Compare eligibility, rates, and features across banks, NBFCs, and digital lenders.

- Prepare Documentation

- Apply Online or Offline:

Submit application and documents through the lender’s channel.

- Credit Evaluation:

Lender assesses credit score, documentation, collateral, and business health.

- Sanction & Disbursal:

Once approved, funds are typically disbursed within a few days.

Government Schemes and Subsidies for Working Capital

Numerous government schemes in India support MSMEs with tailored working capital solutions. Below is a table summarizing key initiatives and their main features for quick reference:

| Scheme / Initiative | Key Features |

|---|---|

| Pradhan Mantri Mudra Yojana | Loans up to ₹10 lakh for MSMEs; no collateral required |

| CGTMSE | Credit guarantee covers up to 85% of loan default risk for eligible MSMEs |

| SIDBI Working Capital Initiatives | Sector-focused schemes for manufacturing, services, and exports |

| Other Specialized Schemes | Dedicated programs for women entrepreneurs, SC/ST MSMEs, and various national priority sectors |

How to Choose the Right Working Capital Loan

- Assess needs: Amount, speed, and purpose of funds.

- Compare lenders: Look at interest rates, processing time, eligibility criteria, and reputation.

- Collateral requirement: Decide if you can/want to pledge assets.

- Repayment flexibility: Match EMIs to your cash flows.

- Review fine print: Processing fees, prepayment charges, hidden costs.

- Digital vs. Traditional: Digital lenders expedite processes but may offer lower limits.

Secured vs. Unsecured Working Capital Loans

| Aspect | Secured Loans | Unsecured Loans |

|---|---|---|

| Backed by | Collateral (property, FDs, assets) | No collateral needed |

| Interest Rates | Lower | Higher |

| Approval Speed | Moderate—valuation of assets needed | Faster |

| Risk/Requirements | Asset risk, possible undervaluation | Higher eligibility criteria, strong credit |

| Best for | Asset-rich, creditworthy businesses | Companies without assets or quick needs |

- Secured loans generally offer better rates but place assets at risk.

- Unsecured loans suit businesses needing quick cash or lacking collateral but often cost more

Key Features & Benefits of Working Capital Loan

- Short Tenure: Usually 3 months to 2 years

- Flexible Repayment: Structure and tenure suited to cash flow cycles

- Minimum or No Collateral: Many new-age lenders offer unsecured loans

- Digital Application: Speedy, paperless processing through online portals

- High Credit Limits: Depending on turnover and creditworthiness

Why Do Indian Businesses Need Working Capital Loans?

- Smooth Daily Operations: Covers recurring expenses even when revenue timing misaligns with payments.

- Cash Flow Stability: Handles operational fluctuations—essential in sectors with seasonal sales.

- Seize Growth Opportunities: Quickly access funds for bulk inventory purchases, new projects, or time-sensitive deals.

- Mitigate Emergencies: Manage unexpected repair, supply chain disruption, or payment delays.

Indian businesses increasingly rely on working capital finance, which constituted 71% of total secured debt in Q4 2023, up from 66% earlier. The MSME sector, in particular, has demonstrated strong growth, securing larger loans and showing improved working capital management year-over-year.

Real-World Example: How a Working Capital Loan Transformed a Business

Let’s look at the case of M/s R K Battery, a microenterprise located in Shivpur, Varanasi, specializing in inverter and battery sales and service.

The Challenge

- Before the loan (2011–2016):

Business growth was stuck due to a lack of funds. M/s R K Battery could not purchase inventory in bulk or expand its customer base, resulting in low annual sales.

The Solution

- In 2016:

The proprietor, Mrs. Nisha Singh, approached a bank for assistance under the Pradhan Mantri Mudra Yojana (PMMY).- She was sanctioned a working capital loan of ₹5 lakh.

How the Loan Helped

- Working capital financing allowed her to:

- Purchase inventory in cash and at a discount, boosting her profit margins.

- Serve both retail and wholesale customers, rapidly expanding her sales network.

- Fulfill bulk orders and consistently supply products, improving her credibility with buyers.

Measurable Results

- Annual sales post-loan (by March 2017):

Jumped to ₹1 crore, a dramatic rise from previous levels. - Employment:

The business expanded and supported 5 employees. - Continued growth:

Impressed by her performance, the bank increased her working capital loan limit to ₹10 lakh in January 2018, supporting further growth, increased inventory, and new customer segments.

Key Numbers

| Item | Before Loan (2016) | After ₹5 lakh Loan (2017) | After Enhanced Limit (2018) |

|---|---|---|---|

| Annual Sales | Low/Undisclosed | ₹1 crore | — |

| Working Capital Loan Limit | ₹0 | ₹5 lakh | ₹10 lakh |

| Employees Supported | Few | 5 | More (after expansion) |

| Customer Base | Limited | Expanded (retail+wholesale) | Further expanded |

Impact

- The working capital loan directly enabled the business to break a low-growth cycle, double down on procurement, and scale up.

- Reliable funds meant no missed business opportunities due to stock-outs or slow fulfillment.

- The business not only grew revenue but also created new jobs and contributed economically to the local community.

This real-world example shows how strategic use of a working capital loan can dramatically accelerate business growth in the Indian MSME space, especially when funds are used efficiently to unlock supply chain and sales opportunities

“Working capital loans help over 60% of Indian MSMEs maintain liquidity during cash flow gaps, enabling timely payments and business growth. At Credit Dharma, we guide businesses to select loans that align with their operational cycles—helping them avoid costly debt traps and improve credit scores, fueling sustainable growth.”

-Sanjay Bharti, Loan Expert, Credit Dharma

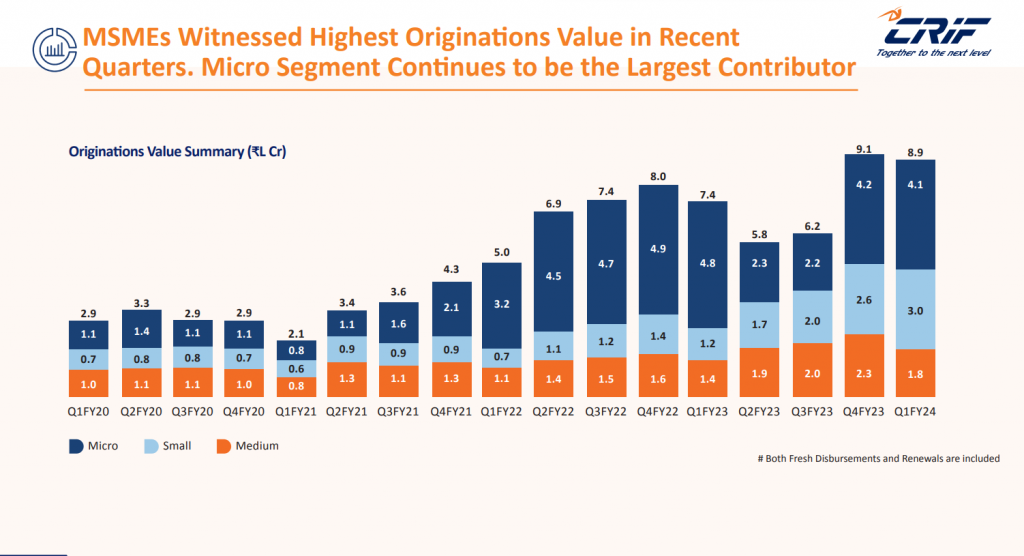

MSME Loan Originations Growth

The attached graph shows the quarterly originations value highlighting the rising demand for MSME and working capital loans across micro, small, and medium enterprises.

Source: CRIF High Mark, How India Lends

Trends in Working Capital Financing in India (2025)

- Rising Demand: Macroeconomic shocks, inflation, and supply chain disruptions increased working capital loan demand by 28% to over ₹11 lakh crore in FY23, with MSME and commodity-intensive sectors most affected.

- Digital Transformation: NBFCs and fintechs provide quick, paperless approvals, driving credit to small businesses.

- Regulatory Push: Government schemes focus on digital KYC, credit guarantee, and broader access.

- Flexible Products: Lenders increasingly offer tailored tenures, top-up facilities, and sector-specific products.

Get the Best Working Capital Loan Offers with Credit Dharma

Credit Dharma is your trusted partner for securing the best loan offers, with over ₹500 Cr+ loans handled and partnerships with 20+ leading banks. We provide exclusive access to the lowest interest rates and a seamless, digital process with fast approvals in just 1-2 weeks, backed by lifetime support from our home loan experts.

Why choose Credit Dharma? We provide:

- Lowest Interest Rates: Save more with every EMI.

- Simple & Digital Process: No tedious paperwork or branch visits.

- Expert Guidance: Lifetime support from our team of specialists.

Compare, choose, and secure the best Working Capital Loan offer with Credit Dharma — your home loan journey starts here!

Conclusion

A working capital loan is a vital resource for Indian businesses to ensure smooth operations and steady cash flow. Understanding your options, eligibility, and government schemes helps you choose the best loan to meet your needs. With flexible terms and quick approvals from trusted banks and NBFCs, working capital loans empower you to grow your business confidently. Secure the right funding today to keep your business thriving in a competitive market.

Frequently Asked Questions

A working capital loan is a short-term business loan designed to provide funds for a company’s daily operations—such as inventory purchase, salaries, and utility bills—rather than for long-term investments or asset purchases. It helps businesses manage cash flow gaps and ensures smooth operations.

Eligible applicants include individuals, proprietors, private/public companies, MSMEs, startups, and self-employed professionals engaged in trading, manufacturing, or services with a minimum operational track record (typically 1–3 years) and a satisfactory credit score.

The most common forms are overdraft facility, cash credit, short-term loans, invoice or bill discounting, trade credit, line of credit, and letter of credit. Each caters to specific operational needs and business profiles.

Many working capital loans, especially from NBFCs and digital lenders, are unsecured and do not require collateral. However, some products (like higher-value or bank-backed loans) may require property, inventory, or receivables as security.

Processing is usually fast—online NBFCs and fintechs often disburse funds within 24–72 hours, provided the documents are in order. Traditional banks may take 2–7 days, especially for larger loans or if collateral evaluation is needed.

Interest rates vary from 10% to 26% (sometimes higher for riskier profiles) and depend on the lender, borrower’s credit profile, and loan type. Repayment tenures usually range from 3 months to 24 months, with some lender flexibility.

Repayment is typically done through monthly EMIs or as per the cash flow cycle of your business. Many lenders offer flexible repayment schedules or revolving credit lines for greater convenience.

Yes; many lenders serve startups, provided the business demonstrates stable cash flow, a sound business model, and sufficient creditworthiness or personal guarantees. Government schemes like Mudra also support new businesses.

Yes. Regular, on-time repayment boosts your business (and sometimes personal) credit score, enhancing eligibility for larger or cheaper loans in future.

Funds can be used for any business operational expense: purchasing inventory or raw materials, paying staff, vendor payments, covering seasonal demand spikes, or managing unforeseen expenses—not for long-term asset acquisition.

HDFC Home Loan

HDFC Home Loan SBI Home Loan

SBI Home Loan