Buying a home has become a bit like a game with two rulebooks: the old one and the new one. These rulebooks are actually tax regimes, and they influence how we handle money, especially when getting a home loan.

The old rules had their ways, but now we’ve got a fresh set to follow. Think of it like an updated playbook. Understanding these changes is crucial, especially if you’re thinking about getting a home loan. It’s not just about forms and numbers; it’s about how these rule changes can impact your journey to owning a home.

Let’s take a closer look at how the old and new tax rules shape the path to getting a home loan.

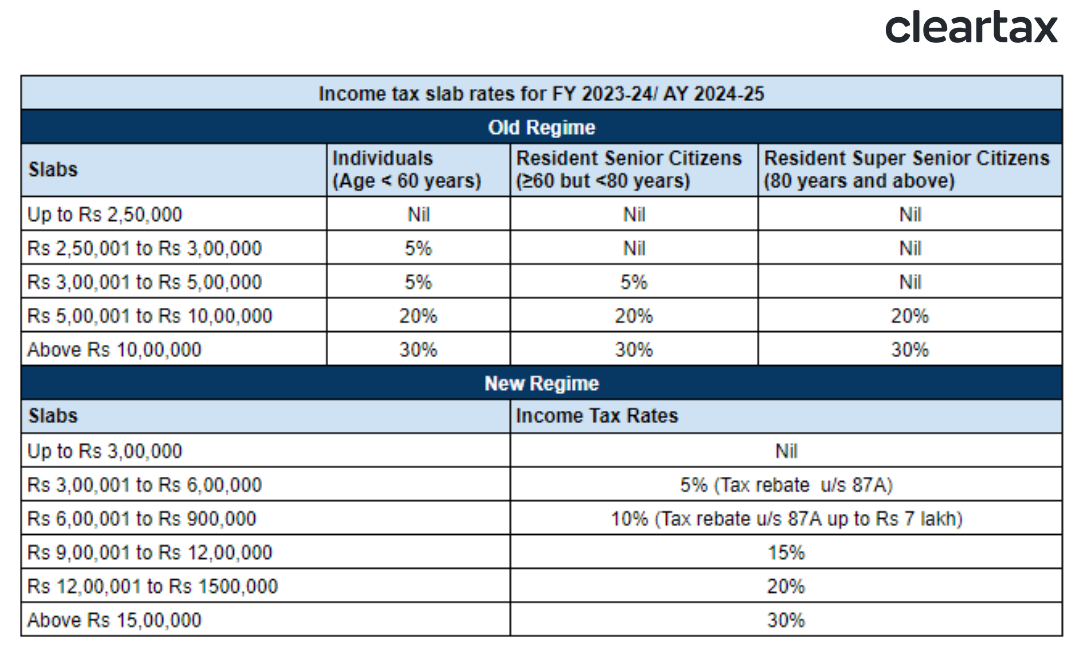

Understanding the Old Tax Regime – The Basics

The old tax regime, characterized by slab-based taxation, featured a progressive structure with distinct income brackets and corresponding tax rates. The slabs were designed to ensure that individuals with higher incomes bore a greater tax burden.

The income slabs typically ranged from lower to higher thresholds, with each slab attracting a specific tax rate. This progressive system aimed to achieve a fair distribution of the tax burden based on one’s ability to pay.

The old tax regime offered various deductions and exemptions to individuals, providing avenues to reduce their taxable income. Notable deductions and exemptions among these were,

- Deductions for House Rent Allowance (HRA),

- Investments under Section 80C,

- Home loan interest under Section 24(b),

- Special provisions like Section 80EE for first-time homebuyers.

These deductions played a pivotal role in minimizing taxable income, offering taxpayers opportunities to optimize their financial planning.

Impact of the old tax regime on home loans

Under the old tax regime, the treatment of home loans had a substantial impact on taxpayers. Home loan interest was eligible for deductions under Section 24(b) of the Income Tax Act. Taxpayers could claim deductions on the interest paid for the home loan, reducing their taxable income.

However, the regime imposed certain maximum limits on these deductions, emphasizing the importance of understanding these limits for effective tax planning. Simultaneously, principal repayment of home loans, typically covered under Section 80C, also offered tax benefits.

Understanding the New Tax Regime – The Basics

The new tax regime brought about significant changes, primarily characterized by simplified tax slabs. Unlike the previous slab-based taxation, the new regime featured a streamlined structure with fewer tax brackets. This simplification aimed to make the tax system more straightforward and user-friendly.

Another notable transformation in the new tax regime was the removal of various exemptions and deductions. This included the elimination of specific tax benefits related to home loans, such as deductions for home loan interest and principal repayment.

Impact of the New Tax Regime on Home Loans

The changes in the new tax regime had a direct impact on the tax benefits associated with home loans. Borrowers must navigate a changed financial landscape, reassessing strategies and optimizing tax liabilities. Existing home loan holders need to adapt to these regulations, emphasizing the need for informed financial planning in this transformed tax environment.

A Comparative Analysis of old vs new tax regime on Home Loans

- Income Tax Slabs: In the old regime, income tax slabs were structured progressively, with varying tax rates for different income brackets. The new regime introduced simplified tax slabs, reducing the number of brackets. For example, the old regime might have had more nuanced slabs at higher income levels, while the new regime streamlined these into broader categories.

- Exemptions and Deductions: Under the old regime, taxpayers enjoyed a plethora of exemptions and deductions, including those related to home loans, HRA, and various investments. In contrast, the new regime aimed for simplicity by removing several exemptions and deductions.

- Home Loan Interest and Principal Repayment: Under the old regime, taxpayers enjoyed deductions on both home loan interest and principal repayment, providing substantial relief. The new regime’s alterations in this regard could impact existing homeowners and prospective buyers, potentially influencing their decisions on real estate investments.

Detailed Real-World Case Studies on Old vs New Tax Regime

Let’s explore real-world scenarios comparing the old and new tax regimes for individuals.

Ananya’s Home Purchase Scenario – Revisited

Meet Ananya, a resident of Delhi working in the fintech sector. She purchased a home using a home loan under the old tax regime, capitalizing on deductions for both home loan interest and principal repayment. With an annual income placing her in the higher tax brackets, Ananya utilized various exemptions to optimize her tax liability.

| Old Tax Regime | New Tax Regime |

| Income | Rs. X (Higher tax brackets) |

| Deductions under Home Loan Interest | Rs. Y (e.g., Interest on Home Loan) |

| Deductions under Section 80C | Rs. Z (e.g., Principal Repayment) |

| Other Exemptions | Rs. W (e.g., HRA, Medical Allowance) |

| Total Deductions and Exemptions | Rs. (Y + Z + W) |

| Taxable Income | Rs. (X – Y – Z – W) |

| Tax Liability (as per applicable rates) | Rs. (Taxable Income * Tax Rate) |

With Old Tax Regime,

- Ananya significantly benefited from deductions on home loan interest, leading to a considerable reduction in her taxable income.

- Deductions under Section 80C for principal repayment played a crucial role in enhancing the affordability of her homeownership.

For instance, If Ananya’s income (X) is Rs. 25,00,000, with Rs. 3,00,000 deductions under home loan interest (Y) and Rs. 2,00,000 under Section 80C for principal repayment (Z), and Rs. 1,00,000 in other exemptions (W), her taxable income under the old regime would be Rs. 19,00,000.

If She Had Decided to Transition to New Tax Regime,

- Challenges arise due to the removal of deductions for home loan interest and principal repayment in the new regime.

- The loss of benefits has a substantial impact on her overall tax liability, prompting Ananya to reevaluate the financial feasibility of maintaining her home.

- The streamlined tax slabs in the new regime introduce uncertainties about the actual impact on her disposable income.

The new regime might have a higher tax rate, resulting in increased tax liability and impacting her disposable income.

Analysis of Various Financial Scenarios

| Regime | Old Regime | New Regime |

| Income | Rs. X | Rs. X |

| Deductions under Section 80C | Rs. Y (e.g., Provident Fund, PPF) | Rs. – (Eliminated under new regime) |

| Other Exemptions | Rs. Z (e.g., HRA, Medical Allowance) | Rs. – (Reduced in the new regime) |

| Total Deductions and Exemptions | Rs. (Y + Z) | – |

| Taxable Income | Rs. (X – Y – Z) | Rs. X |

| Tax Liability (as per applicable rates) | Rs. (Taxable Income * Tax Rate) | Rs. (X * New Tax Rate) |

Scenario 1: Middle-Income Individual – Revisited

Consider Mr. Sahara, a middle-income individual without a home loan. Under the old regime, he benefited from deductions under Section 80C and other exemptions. Transitioning to the new regime, Mr. Saharacmight experience a reduction in overall tax liability due to the simplified structure, provided he does not heavily rely on the eliminated deductions.

If Mr. Sahara’s income (X) is Rs. 10,00,000, with Rs. 1,50,000 deductions under Section 80C (Y) and Rs. 50,000 in other exemptions (Z), his taxable income under the old regime would be Rs. 8,00,000. The new regime might have a lower tax rate, resulting in reduced tax liability.

Scenario 2: High-Income Individual with Investments – Revisited

Now, let’s examine Nihara, a high-income individual who heavily invested under Section 80C in the old regime. Despite losing certain deductions, the new regime might still offer advantages due to lower tax rates for higher income slabs. Nihara’s financial portfolio restructuring could optimize her tax liability.

If Nihara’s income (A) is Rs. 20,00,000, with Rs. 2,00,000 deductions under Section 80C (B) and Rs. 1,00,000 in other exemptions (C), her taxable income under the old regime would be Rs. 17,00,000. The new regime might have a lower tax rate, resulting in reduced tax liability.

Scenario 3: First-Time Homebuyer – Revisited

Consider Priyansh, a first-time homebuyer in Mumbai. Under the old regime, he enjoyed deductions under Section 80EE. The transition to the new regime might pose challenges, impacting the financial feasibility of his home purchase. However, if Priyansh falls within lower tax brackets, the simplified structure might still benefit him.

If Priyansh’s income (P) is Rs. 12,00,000, with Rs. 1,50,000 deductions under Section 80EE (Q) and Rs. 60,000 in other exemptions (R), his taxable income under the old regime would be Rs. 10,90,000. The new regime might have a lower tax rate, resulting in reduced tax liability.

Financial Planning Tips with Credit Dharma

As both homeowners and taxpayers navigate the challenges and opportunities presented by shifting tax regimes, a proactive and informed approach to financial planning becomes paramount. Professional advice, continuous education on tax laws, and strategic decision-making based on individual financial goals contribute to optimizing tax liabilities and achieving long-term financial well-being.

If you are taking a home loan, you must seek advice from Credit Dharma, an innovative financial advisory solution. Their team of experts ensures advantageous mortgage terms, providing low processing fees, personalized prepayment plans, and efficient loan processing.

Professional Guidance – Why Choose Credit Dharma?

When you choose Credit Dharma, you can optimize your home loan savings, attain quicker loan freedom, and benefit from a comprehensive solution for all your housing finance requirements, with their unique tips and strategies.

You will get,

- Competitive Home Loan Interest Rates: You can benefit from low-interest rates starting at 8.4% p.a.. It provides a cost-effective solution to reduce your overall Home Loan expenses.

- Swift Loan Disbursal: You will experience expedited loan disbursal. It ensures prompt progress with your home plans without unnecessary delays.

- Lifetime Support: You will enjoy complimentary lifelong expert support from them. Their dedicated team is always ready to assist you at every stage of your home loan journey.

- Spam-Free Experience: At Credit Dharma, your privacy is highly valued and you don’t have to worry about spam or unwanted communications from vendors.

Opting for a home loan with Credit Dharma is very simple. You just have to input your loan details, choose your preferred property amount and city, and Credit Dharma will assist in assessing your home loan eligibility. It ensures a streamlined and cost-effective journey toward homeownership. You can explore Credit Dharma’s home loan eligibility calculator to determine the loan amount you are eligible for based on your income.

Conclusion – Take the Decision with Proper Planning

The debate between the old and new tax regimes has significant implications for individuals seeking home loans. The choice between these regimes involves a careful consideration of various factors, including income levels, individual preferences, and long-term financial goals.

The old tax regime, with its numerous deductions and exemptions, may appeal to those who prioritize immediate tax savings and have a diverse portfolio of investments. On the other hand, the new tax regime offers simplicity and transparency, streamlining the tax structure but potentially reducing certain tax benefits.

In the context of home loans, the impact of the tax regime choice is substantial. Homebuyers must weigh the advantages of deductions like interest payments and property taxes available under the old regime against the simplicity and lower tax rates offered by the new regime.

FAQs

What are the key differences between the old and new tax regimes affecting home loans?

The key differences between the old and new tax regimes include revised tax slabs, deductions, and exemptions affecting home loans.

Are there specific advantages or disadvantages for home loan seekers in the new tax regime compared to the old one?

The new tax regime may offer advantages like simplified tax structures but could also bring disadvantages concerning reduced exemptions impacting home loan seekers.

Can existing home loan holders benefit from the changes in the tax regime, and how should they navigate these changes?

Existing home loan holders may benefit from reviewing their financial plans, exploring new deductions, and adjusting strategies based on changes in the tax regime.

HDFC Home Loan

HDFC Home Loan SBI Home Loan

SBI Home Loan