Managing your monthly EMI payments efficiently is crucial to maintaining a good credit standing and ensuring that your loan tenure proceeds smoothly. IDFC FIRST Bank offers multiple convenient payment methods—ranging from automated transactions to in-person cash deposits—to help you repay your home loan on time.

EMI Dates and Structure

Your home loan EMIs at IDFC FIRST Bank are scheduled on the 3rd and 5th of every month. Each EMI consists of two components:

- Principal: The portion that pays down the loan balance.

- Interest: The cost you pay to borrow the principal.

With every payment you make, your outstanding loan amount decreases and you move one step closer to fully repaying your loan.

1. Auto-Debit (SI/E CS) Facility

The simplest way to ensure timely payments is to set up an automatic debit from your bank account.

- What It Is: By authorizing IDFC FIRST Bank, your EMI will be automatically deducted from your designated account each month on the scheduled date.

- Benefits:

- No need to remember due dates.

- Eliminates the risk of late fees or missed payments.

- How to Set It Up:

- Contact IDFC FIRST Bank’s customer service to activate the bank mandate.

- Provide your account details and necessary authorization.

- Once set up, the EMI amount will be auto-debited every month.

Read More: Home Loan Repayment Strategies

2. Online Repayment Through Net Banking, Debit Card, UPI, or Digital Wallets

If you prefer to manually pay each month while enjoying the flexibility of doing so at your convenience, online channels are ideal.

Step-by-Step Process:

- Visit the Payment Portal: Go to the IDFC FIRST Bank’s quick pay EMI page.

- Enter Your Details: Input your Loan Account Number (LAN) or your registered mobile number and date of birth to fetch your loan details.

- Select Payment Option: Choose from available gateways like Billdesk, Paytm, Mpesa, or UPI. Enter the CAPTCHA code and click on “Proceed Next.”

- Review Loan Details: Verify your loan account details and input the amount you wish to pay, then click on “Proceed.”

- Make the Payment: You’ll be redirected to the bank’s secure payment page. Choose your preferred method—Net Banking, Debit Card, Wallet, or UPI—and enter the required details to complete the transaction.

Check Out: IDFC Home Loan EMI Calculator

3. Payment at IDFC FIRST Bank Branches

For those who prefer face-to-face transactions, you can make your EMI payments at any IDFC FIRST Bank branch.

- Visit the Nearest Branch: Locate your closest branch on the IDFC FIRST Bank website or app.

- Carry Your LAN: Your Loan Account Number (LAN) is crucial for identification. It’s provided in SMS communications from IDFC FIRST Bank.

- Provide Details to the Service Desk: Share your LAN, Customer Name, Date of Birth, and Registered Mobile Number.

- Complete the Payment: You can pay using cash, cheque, Demand Draft (DD), or debit card. Once done, the bank will issue an e-receipt via SMS or email for your records.

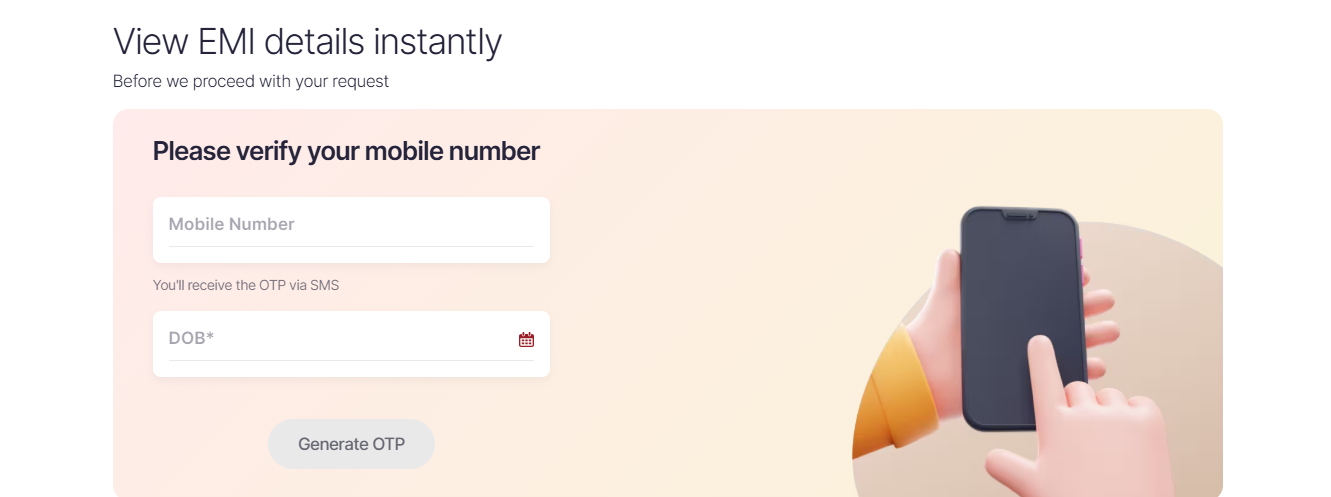

How to View Your IDFC First Bank Home Loan EMI Details Instantly?

- Visit the IDFC First Bank EMI Details page.

- Enter your mobile number and date of birth.

- Click on the “Generate OTP” button. You will receive a One-Time Password (OTP) on your registered mobile number via SMS.

- After successful verification, your EMI details will be displayed on the screen.

Tips for Hassle-Free EMI Management

- Set Reminders: Even if you use auto-debit, keeping personal reminders ensures you monitor your account balance before EMI dates.

- Check Bank Statements: Regularly verify that your EMIs are debited correctly.

- Maintain Sufficient Balance: If you opt for auto-debit, ensure your account has enough funds on the EMI date to avoid penalties.

- Keep Records: Always save or note down your transaction IDs, SMS confirmations, and e-receipts for future reference.

Conclusion

IDFC FIRST Bank provides multiple channels to pay your home loan EMIs, giving you the freedom and flexibility to choose the method that best suits your lifestyle.

By choosing the right EMI payment mode and staying consistent, you not only avoid late fees and penalties but also maintain a strong credit profile, ensuring a smoother financial journey throughout the tenure of your home loan.

Frequently Asked Questions

Missing an EMI may attract late payment charges, impact your credit score, and increase your loan burden due to accrued interest.

Generally, home loan EMI dates are fixed (e.g., 3rd or 5th of every month). However, you can contact your lender to check if a change is possible based on bank policies.

You can repay your home loan EMIs through:

Auto-debit (ECS/SI facility)

Online payments via Net Banking, UPI, or Debit Card

Cash, cheque, or DD at the bank branch

Yes, most banks allow partial prepayment or foreclosure of home loans. Some may charge a prepayment penalty, especially for fixed-rate loans.

EMI: Starts after the loan is fully disbursed and includes both principal and interest.

Pre-EMI: Paid during the loan disbursement phase (e.g., construction stage) and only covers the interest component.

HDFC Home Loan

HDFC Home Loan SBI Home Loan

SBI Home Loan