Are you considering a home loan but want more flexibility with your repayments? Our Home Loan Overdraft Calculator helps you calculate the exact savings and tax benefits of an OD facility on your loan account.

A home loan with an overdraft facility might be the perfect solution for you.

This comprehensive guide explores everything you need to know about home loan overdraft facilities in India – from how they work to their benefits, drawbacks, and how to choose the best option for your needs.

Save on 30+ Home Loan EMIs with Overdraft Facility

What is a Home Loan Overdraft Facility?

A home loan overdraft facility is an innovative lending product that combines the features of a traditional home loan with the flexibility of an overdraft account.

Simply put, it links your home loan to a current account, allowing you to deposit surplus funds into the account and withdraw them when needed, all while reducing your interest payments on the outstanding loan amount.

Unlike a traditional home loan, where your EMI remains constant throughout the loan tenure (unless you make prepayments), a home loan with an overdraft facility calculates interest only on the net outstanding amount after considering deposits made into the linked account.

Expert Insight: “Home loan overdraft facilities are particularly beneficial for borrowers with irregular income patterns or those who receive occasional lump sums. It provides flexibility while optimizing interest costs.” – Rajiv Kumar, Senior Banking Consultant with 15+ years of experience in mortgage products.

Which Banks in India Have an Overdraft Facility for Home Loans?

Several leading banks and housing finance companies in India offer home loans with overdraft facilities, each with its own set of features and conditions. Here are some prominent options:

Here are the key details for Home Loans with Overdraft offered by the banks mentioned, covering interest rates, eligibility, documents required, processing fees, and other charges:

Summary Table for ICICI, PNB, and HDFC Home Loans With Overdraft Facility (where detailed info is available)

| Bank | Interest Rate | Eligibility | Processing Fee | Documents Required | Other Charges/Notes |

|---|---|---|---|---|---|

| ICICI Bank | 8.70% – 9.55% p.a. (floating, based on credit score) | All profiles including companies | Linked to home loan rates, approximately. 8.5% – 9.5% p.a. | Standard home loan docs; no extra for OD | Commitment fee 0.5% if <30% utilization (not salaried); renewal ₹5,000 |

| PNB (Max Saver Housing Loan) | Floating: 8.00% – 9.85% p.a.; Fixed: 9.00% – 11.35% p.a. | Existing/fresh housing loan borrowers | Nil for OD | Housing loan docs or request letter for existing loans | OD limit 2L-25L; must service interest monthly |

| HDFC Bank | 8.70% – 9.55% p.a. (floating, based on credit score) | ₹50,000 to ₹10 lakh; MSMEs eligible | PAN, Aadhaar, income proof, and address proof | PAN, Aadhaar, income proof, address proof | No prepayment or renewal fees; 24% p.a. if over limit utilized |

Sources of Information:

- ICICI Home Loan with Overdraft Facility – Interest Rates and Other Details | Official ICICI Website

- PNB Max Saver Housing Loan – Interest Rates and More Details | PNB’s Official Website

- HDFC Home Loan Overdraft For Business Expansion – Interest Rates and More Details | HDFC Bank’s Official Website

Detailed Overview of All Indian Banks Offering Home Loans with Overdraft Facility:

1. ICICI Bank Home Loan Overdraft

- Interest Rates: Interest charged only on the utilized amount; specific rates vary by profile and loan type.

- Eligibility: All profiles, including proprietorship, partnership, LLPs, private and public limited companies, trusts, and societies.

- Documents Required: Standard home loan documents including property papers, facility agreement, disbursement request, repayment mandate, and other legal clearances. No additional documents specifically for overdraft beyond home loan documentation.

- Processing Fees & Charges:

- Processing fee up to 2% of the loan amount (non-refundable).

- Administrative charges 0.25% of the facility amount or ₹5,000, whichever is lower.

- Commitment charges/non-utilization fee: 0.5% on the deficit amount if utilization is below 30% quarterly (not applicable for salaried customers).

- No prepayment fees.

- Other charges include penal charges on overdue, cheque bounce charges, and renewal fees of ₹5,000 for the overdraft product.

- Other Features: Combination of term loan and overdraft in any proportion; reverse sweep facility; overdraft can be taken as top-up or against various property types.

2. Punjab National Bank (PNB) Housing Overdraft

- Interest Rates: Linked to housing loan rates; specifics depend on loan terms.

- Eligibility: Borrowers with existing or fresh housing loans for purchase, construction, repair, or renovation. Not eligible if construction is incomplete on the plot.

- Documents Required: Same as housing loan; for existing loans, a request letter and acceptance of terms suffice.

- Processing Fees & Charges: Nil processing fees for overdraft; only extension or creation of a charge on the mortgaged property.

- Overdraft Limits:

- Minimum Rs. 2 lakh, maximum Rs. 25 lakh.

- Up to 80% of realizable property value if total exposure ≤ Rs. 75 lakh; 75% if above Rs. 75 lakh.

- Other Conditions: Interest servicing is mandatory monthly; overdraft can continue after full repayment of the housing loan.

3. HDFC Bank Home Loan Overdraft

- Interest Rates: Charged only on utilized amount; linked to HDFC’s Retail Prime Lending Rate (RPLR); typically 15%-18% p.a.

- Eligibility: Loan amount from ₹50,000 to ₹10 lakh; MSMEs with 6+ years in business may qualify.

- Documents Required: PAN card, Aadhaar, proof of address, income proof (salary slips, bank statements), business proof for self-employed.

- Processing Fees & Charges:

- Processing fee up to 1% of the loan amount.

- No prepayment or annual renewal charges.

- Stamp duty and statutory charges as per state law.

- Interest rate of 24% p.a. on the amount utilized beyond the overdraft limit.

- Other Features: Flexibility to deposit surplus funds to reduce interest; withdraw anytime, no collateral required for overdraft facility.

- Application: Can be applied online or via phone; funds disbursed quickly.

4. Axis Bank Home Loan Overdraft

- Typically offers an overdraft linked to a home loan with competitive interest rates and flexible repayment.

- Eligibility and documentation usually align with standard home loan norms.

- Processing fees and charges vary; they generally include a processing fee and interest on the utilized amount.

5. IDBI Bank Home Loan Overdraft

- Offers overdraft against property security.

- Eligibility includes salaried/self-employed individuals with a minimum monthly income of around Rs. 25,000.

- Interest is charged only on the utilized amount.

- Processing fees and other charges depend on loan terms.

6. State Bank of India (SBI) Home Loan Overdraft

- Overdraft against property security, interest on the utilized amount.

- The property must be in the borrower’s name and located in a city with a population of over 1 lakh.

- Standard home loan documentation and eligibility apply.

7. Central Bank of India Home Loan Overdraft

- Overdraft facility aimed at efficient cash flow and minimizing interest burden.

- Eligibility and documentation as per housing loan norms.

8. Bank of India Home Loan Overdraft

- Includes cheque book, debit card, and net banking for overdraft operation.

- No prepayment penalty.

- Standard home loan eligibility and documentation.

Comparison of Different Home Loan Overdraft Products (Rates, Fees, Hidden Charges)

When comparing home loan overdraft products, it’s essential to look beyond just the interest rates. Here’s a detailed comparison of key aspects:

Processing Fees and Charges

| Bank | Processing Fee | Account Maintenance Fee | Foreclosure Charges | Withdrawal Restrictions |

|---|---|---|---|---|

| SBI | 0.35% (Min: ₹2,000, Max: ₹10,000) | Nil for first year, ₹1,000 per annum thereafter | Nil after 6 months | No minimum balance requirement |

| ICICI Bank | Up to 1% of loan amount | ₹500 per quarter | Nil after 6 months | Minimum withdrawal ₹25,000 |

| HDFC Bank | Up to 1% of the loan amount | ₹600 per quarter | Nil after 6 months | Minimum withdrawal ₹25,000 |

| Axis Bank | 1% of loan amount | ₹750 per quarter | 2% for first 3 years, nil thereafter | Minimum withdrawal ₹50,000 |

| Citibank | Up to 1% of loan amount | ₹500 per month | 1% for the first 2 years, nil thereafter | Minimum withdrawal ₹50,000 |

| Bank of Baroda | 0.50% of loan amount | ₹500 per quarter | Nil after 1 year | Minimum withdrawal ₹25,000 |

| Kotak Mahindra Bank | Up to 0.50% of the loan amount | ₹750 per quarter | 2% for the first 2 years, nil thereafter | Minimum withdrawal ₹25,000 |

Hidden Charges to Watch Out For

- Switching Fees: Some banks charge a fee for switching from a regular home loan to an overdraft facility.

- Documentation Charges: Additional charges for documentation when setting up the overdraft facility.

- Cheque Bounce Charges: Higher penalties for insufficient funds in overdraft accounts.

- Statement Charges: Some banks charge for physical statements of the overdraft account.

- Inactivity Fees: Charges are applicable if the overdraft feature is not utilized for a certain period.

- Conversion Fees: Fees for converting between different interest rate options (fixed to floating or vice versa).

Expert Warning: “Always read the fine print and ask specifically about hidden charges. Banks sometimes bury important fee information in lengthy terms and conditions documents.” – Priya Sharma, Consumer Banking Rights Advocate

How Does an Overdraft Facility Work in the Indian Banking System?

In the Indian banking system, a home loan overdraft facility typically operates through these mechanisms:

- Linked Account Setup: The bank creates a current account or overdraft account linked to your home loan.

- Deposit Flexibility: You can deposit surplus funds into this account at any time.

- Interest Calculation: Interest is calculated only on the effective outstanding loan amount (principal loan amount minus the balance in your linked account).

- Withdrawal Rights: You can withdraw the deposited surplus funds whenever needed without any prepayment penalties.

- EMI Consistency: Your EMI typically remains the same, but a larger portion goes toward principal repayment when you maintain higher balances in the linked account.

Example Scenario: Let’s say you have a home loan of ₹50 lakhs. With a traditional home loan, you’ll pay interest on the entire outstanding amount. However, with an overdraft facility, if you deposit ₹10 lakhs from your bonus into the linked account, you’ll only pay interest on ₹40 lakhs until you withdraw that money.

What are the Eligibility Criteria for Getting a Home Loan with an Overdraft Facility in India?

Who Qualifies for a Home Loan Overdraft?

Banks typically have specific eligibility criteria for home loan overdraft facilities. These are generally more stringent than for regular home loans:

- Age: The applicant’s age should typically be between 24 and 65 years at the time of loan commencement and maturity, respectively.

- Employment Status: Both salaried professionals and self-employed individuals can apply. Salaried applicants should be in permanent service in a reputed company or government, while self-employed individuals must file Income Tax returns regularly. Professionals like doctors, engineers, CAs, etc., are also eligible.

- Existing Home Loan: Usually, the overdraft facility is offered to existing home loan customers who have taken a home loan against a housing property. Some lenders may allow the facility at the time of fresh home loan sanction as well.

- Credit Score: A good credit score, typically 750 or above, is required to demonstrate creditworthiness and reliable repayment history.

- Income Stability and Repayment Capacity: Applicants must have a stable and regular income, with proof such as salary slips or income tax returns. The ability to service interest on the overdraft is assessed, including co-borrowers’ income and rental income if any.

- Property Requirements: The property against which the loan is taken should be approved by the lender and meet their criteria. The overdraft limit is linked to the realizable value of the mortgaged property, generally maintaining a Loan-to-Value (LTV) ratio of 75-80%.

- Loan Amount and Limits: The overdraft limit is usually a portion of the home loan amount or property value, often around 25% of the loan amount, with minimum and maximum limits varying by lender (e.g., Rs. 2 lakh to Rs. 25 lakh or higher).

- Documentation: Standard documents required include proof of identity, age, income, residence, property documents, bank statements, employment/business proof, credit history, photographs, and a duly filled application form.

- Other Conditions: The overdraft facility is generally not sanctioned for loans taken for the purchase of plots where construction is incomplete. Interest servicing on the overdraft must be maintained regularly, or the bank may recall the loan.

What are the Documents that are Needed for a Successful Home Loan Overdraft Application?

The documentation required for a home loan overdraft facility includes all regular home loan documents plus some additional ones:

| Type of Documents | List of Key Required Documents |

|---|---|

| Identity and Address Proof | – Aadhaar Card – PAN Card – Passport/Voter ID/Driving License – Recent utility bills for address verification |

| Income Documentation | – Last 3 months’ salary slips (for salaried) – Form 16 or Income Tax Returns for the last 2-3 years – Bank statements for the last 6 months – Business financial statements (for self-employed) – GST returns (for business owners) |

| Property Documentation | – Sale deed – Property registration documents – NOC from the housing society/builder – Property tax receipts – Approved building plan |

| Additional Documents for Overdraft Facility | – Current account opening forms – Overdraft facility application – Declaration of fund usage intentions – CIBIL score authorization – Net worth statement (for high-value loans) |

Source of Information: Overdrafts on Home Loans: Eligibility, Benefits & Hidden Risks!

How Long Does it Take For a Home Loan with an Overdraft Facility Approval Process?

The approval process for a home loan with an overdraft facility typically takes longer than a regular home loan due to the additional scrutiny involved:

- Application Submission: 1 day

- Document Verification: 3-5 working days

- Property Legal Verification: 7-10 working days

- Technical Valuation: 2-3 working days

- Credit Appraisal: 3-5 working days

- Final Approval: 2-3 working days

- Loan Agreement and Disbursement: 3-5 working days

- Overdraft Account Setup: 2-3 working days

Total Timeline: Typically 21-35 days (compared to 15-21 days for regular home loans)

Insider Tip: “Submit all documents in one go and maintain regular follow-ups with your relationship manager to expedite the process. Also, applying through your existing bank can significantly reduce the processing time.” – Banking Operations Manager with a leading private bank

Comparing Loan Overdraft Facility with Other Options

An overdraft facility often offers added payment and financial flexibility for managing your debt accounts.

In this section, we will compare a loan overdraft account with the more prevalent loan repayment alternatives and understand the key advantages of an overdraft account:

Overdraft vs Prepayment

| Feature | Home Loan Overdraft | Prepayment |

|---|---|---|

| Interest Savings | Usually, no additional fees | Permanent reduction in loan amount |

| Access to Funds | Can withdraw deposited funds | Once prepaid, funds cannot be accessed |

| Processing Fee | Additional setup and maintenance fees | People with variable income or a need for liquidity |

| Tax Benefits | May impact Section 24 benefits for interest | No impact on tax benefits |

| Flexibility | High flexibility with fund management | No flexibility once prepaid |

| Ideal For | Based on the daily balance in the linked account | Those with stable income and no anticipated need for funds |

| Interest Rate | Slightly higher base rate (0.25-0.5%) | Standard home loan rate |

| Effect on EMI | EMI remains the same, tenure may reduce | Based on the daily balance in the linked account |

When to Choose Overdraft: Choose overdraft if you need flexibility to access your funds in the future or have irregular income patterns.

When to Choose Prepayment: Choose prepayment if you have surplus funds that you’re confident you won’t need in the future and want to permanently reduce your loan burden.

Overdraft vs Loan Against Property

| Feature | Home Loan Overdraft | Loan Against Property |

|---|---|---|

| Purpose | Original home purchase with withdrawal flexibility | Separate loan using existing property as collateral |

| Interest Rate | 8.75% – 9.90% | 9.50% – 12.00% |

| Tax Benefits | Available for home purchase component | Not available for personal use of funds |

| Processing Time | Integrated with a home loan | Separate approval process |

| Usage Restrictions | No restrictions on withdrawn funds | Sometimes has end-use restrictions |

| Effect on Original Loan | Linked to an outstanding home loan | Separate loan in addition to the existing home loan |

| Loan Amount | Same as a home loan | Up to 60-70% of property value |

| Loan Tenure | Separate loan in addition to the existing home loan | Usually 5-15 years |

When to Choose Overdraft: Choose overdraft if you’re at the stage of purchasing a home and anticipate needing flexible access to funds in the future.

When to Choose a Loan Against Property: Choose a loan against property if you already have a regular home loan, have built up equity in your property, and need a large sum for a specific purpose.

Overdraft vs Top-Up Loan

| Feature | Home Loan Overdraft | Top-Up Loan |

|---|---|---|

| Accessibility | Can deposit and withdraw multiple times | One-time additional loan amount |

| Interest Rate | Interest only on net outstanding (original loan minus deposits) | Fixed additional loan amount with interest |

| Processing | Part of the initial setup or conversion | Additional application and processing |

| Flexibility | High flexibility with fund management | No flexibility once disbursed |

| Interest Calculation | Daily reducing balance on the net amount | EMI based on the additional loan amount |

| Tax Benefits | Potentially reduced Section 24 benefits | Additional tax benefits if used for home improvement |

| Tenure | Same as the original home loan | Can have a different tenure than the original loan |

| Processing Fee | 0.5-1% of the loan amount + maintenance fees | 0.5-1% of the top-up amount |

When to Choose Overdraft: Choose overdraft if you need ongoing flexibility to deposit and withdraw funds multiple times.

When to Choose Top-Up: Choose top-up if you need a specific additional amount for a one-time expense and don’t anticipate needing flexible access to funds in the future.

Overdraft vs Personal Loan

| Feature | Home Loan Overdraft | Personal Loan |

|---|---|---|

| Interest Rate | 8.75% – 9.90% | 10.50% – 18.00% |

| Collateral | Home as collateral | No collateral required |

| Processing Fee | 0.5-1% + maintenance fees | 1-3% of the loan amount |

| Access to Funds | Flexible deposit and withdrawal | One-time disbursement |

| Loan Amount | Linked to the home loan outstanding | Based on income and credit score (typically lower) |

| Tax Benefits | Potential home loan tax benefits | No tax benefits |

| Tenure | Same as a home loan | Usually 1-5 years |

| Processing Time | Longer (if setting up new) | Quicker (sometimes same-day approval) |

When to Choose Overdraft: Choose overdraft for larger amounts, lower interest rates, and flexible access if you already have or are applying for a home loan.

When to Choose a Personal Loan: Choose a personal loan for quick access to smaller amounts when you don’t have a home loan or don’t want to link additional debt to your property.

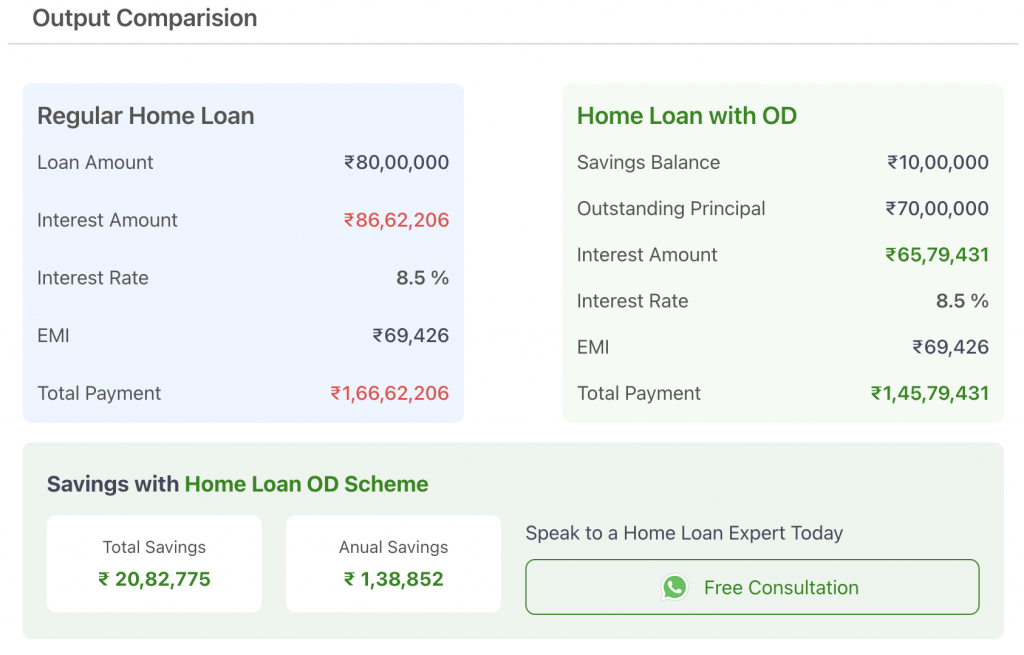

Why Should You Use A Home Loan Overdraft Calculator?

Using a home loan overdraft calculator is beneficial because it helps you understand and optimize the financial advantages of a home loan with an overdraft (OD) facility. Here are the key reasons why you should use one:

- Estimate Interest Savings: The calculator shows how depositing surplus funds into the overdraft-linked account reduces your outstanding principal, thereby lowering the interest you pay over the loan tenure. You can see how additional lump sum deposits impact your EMI and total interest cost.

- Plan Loan Repayment Flexibly: It helps you visualize the effect of making irregular or additional payments without committing to fixed prepayment schedules. Since funds in the overdraft account can be withdrawn anytime, the calculator can model this liquidity and flexibility.

- Compare Scenarios: You can compare the cost-effectiveness of a home loan with an overdraft facility versus a conventional home loan, considering the slightly higher interest rate charged on OD loans. This helps decide if the OD facility suits your financial situation, especially if you have regular surplus funds to deposit.

- Manage Cash Flow: For borrowers with fluctuating income or irregular cash flows, the calculator assists in planning how best to use the overdraft facility to reduce interest while maintaining liquidity for emergencies or other expenses.

Source of Information: Should You Opt for a Home Loan With an Overdraft Facility? | Kotak Mahindra Bank.

How to Use Credit Dharma’s Home Loan Overdraft (OD) Calculator?

Gather your loan details

Before you begin, make sure you have all the necessary details of your home loan at hand. This includes your loan amount, interest rate, loan term, and any additional repayments you’re currently making or planning to make.

Input your Loan Amount

Enter the total amount of your home loan into the overdraft calculator. This should be the principal amount you borrowed or currently owe.

Specify the interest rate

Input the annual interest rate of your home loan. If you have a variable rate, use your current rate or the average rate you expect over the loan term.

Loan Term

Enter the original term of your home loan, typically in years.

Overdraft Details

Enter the amount you plan to deposit into the overdraft account above your regular home loan repayments on a monthly basis.

Analyze the results

After inputting all the required information, the calculator will show you how the additional repayments will affect your loan. Look for the new estimated payoff date, the total interest saved, and how much sooner you could be debt-free. This is similar to how an OD EMI calculator works.

Adjust and Experiment

One of the great features of an OD calculator is the ability to adjust your extra repayment amounts. This is to see how even small changes can have a big impact over time. Experiment with different figures to find a balance that works for your budget and financial goals.

Benefits Of Using an Overdraft Facility Calculator

| Benefit | Description |

|---|---|

| Interest Savings | By making extra repayments into your overdraft account, you reduce the principal balance faster, thereby saving on interest costs over the life of the loan. |

| Flexibility | The overdraft facility allows you to access additional funds up to a pre-approved limit, offering flexibility for unexpected expenses or investment opportunities. |

| Financial Planning | Using an Overdraft Facility Calculator helps in effective financial planning by providing a clear picture of how additional repayments impact your loan term and interest. |

| Budget Management | It encourages better budget management by showing the benefits of allocating extra funds towards your home loan, helping you make informed decisions about your finances. |

| Customized Scenarios | The calculator allows you to input different repayment scenarios, helping you understand the impact of various financial strategies on your home loan. |

| Debt Reduction | By effectively using the overdraft facility, you can reduce your overall debt level faster, leading to financial freedom sooner. |

| Cost Transparency | The calculator provides transparency about the costs associated |

Use-Cases for a Home Loan Overdraft Account

Overdraft for Business Needs

A home loan overdraft facility can be particularly beneficial for business owners and entrepreneurs:

Ideal Business Scenarios:

- Managing Cash Flow Fluctuations: Use the overdraft to cover operational expenses during lean business periods.

- Opportunity Investment: Quick access to capital for unexpected business opportunities without lengthy loan approvals.

- Business Expansion: Fund business growth without applying for a separate business loan.

- Inventory Purchase: Access funds for bulk inventory purchases when suppliers offer discounts.

- Equipment Acquisition: Finance essential equipment purchases while maintaining cash reserves.

Benefits for Business Owners:

- Lower interest rates compared to business loans (8.75-9.90% vs 12-16% for business loans)

- No additional credit assessment for fund access

- Flexibility to withdraw and repay based on business cycles

- Potential tax benefits if the home loan is for a self-occupied property

Real Example:

Sanjay, an e-commerce business owner from Delhi, used his home loan overdraft facility to stock up on inventory before the Diwali season.

He withdrew ₹15 lakhs in September, made ₹22 lakhs in sales during the festive season, and deposited ₹18 lakhs back into his overdraft account by December – saving over ₹25,000 in interest compared to taking a separate business loan.

Overdraft for Home Renovation

Home renovation is one of the most common uses for a home loan overdraft facility:

Renovation Scenarios:

- Major Structural Changes: Funding for adding rooms, floors, or structural modifications.

- Kitchen and Bathroom Remodels: Access funds for high-value upgrades.

- Energy Efficiency Upgrades: Finance solar panels, energy-efficient appliances, or insulation improvements.

- Landscaping and Exterior Work: Fund outdoor improvements that enhance property value.

- Smart Home Conversions: Finance technological upgrades to your property.

Benefits of Opting for an Overdraft Facility for House Renovation:

- Potential tax benefits under Section 24 for home improvement (consult a tax advisor)

- Ability to phase renovations according to funding availability

- Flexibility to adjust renovation budgets as projects progress

- Can increase property value, potentially offsetting interest costs

Cost-Benefit Analysis Example:

| Renovation Project | Estimated Cost | Potential Property Value Increase | Overdraft Interest (1 year) | Net Benefit |

|---|---|---|---|---|

| Kitchen Remodel | ₹7 Lakhs | ₹10-12 Lakhs | ₹63,000-69,300 | ₹2.37-4.37 Lakhs |

| Adding a Bedroom | ₹12 Lakhs | ₹15-20 Lakhs | ₹1.08-1.19 Lakhs | ₹1.92-6.92 Lakhs |

| Bathroom Upgrade | ₹4 Lakhs | ₹5-6 Lakhs | ₹36,000-39,600 | ₹0.64-1.64 Lakhs |

| Solar Panel Installation | ₹3.5 Lakhs | ₹2 Lakhs + ₹36,000/year savings | ₹31,500-34,650 | Break-even in ~5 years |

Overdraft for Major Life Events

The flexibility of a home loan overdraft facility makes it ideal for funding significant life events:

For Weddings

Wedding Expense Management:

- Access funds for venue booking, catering, and other significant upfront costs

- Withdraw only what’s needed as expenses arise

- Replenish the account as wedding gifts and contributions come in

- Avoid high-interest personal loans or credit card debt for wedding expenses

Strategic Approach:

The Kumar family used their home loan overdraft to fund their daughter’s wedding. They withdrew ₹10 lakhs in phases over three months, coordinating with vendor payment schedules. After the wedding, they deposited ₹4 lakhs received as gifts back into the account, immediately reducing their interest burden.

For Education

Education Funding Benefits:

- Finance higher education with interest rates much lower than education loans (8.75-9.90% vs 11-15%)

- Withdraw funds as per the semester fee schedules

- Deposit scholarship amounts or part-time income back into the account

- Flexibility to adjust to changing education expenses

Tax Efficiency: Unlike dedicated education loans, the overdraft facility does not offer specific education loan tax benefits under Section 80E. However, the significantly lower interest rate often compensates for this disadvantage.

Comparison with Education Loan:

| Feature | Home Loan Overdraft | Education Loan |

|---|---|---|

| Interest Rate | 8.75% – 9.90% | 11.00% – 15.00% |

| Tax Benefit | No specific education tax benefit | Tax deduction under Section 80E |

| Loan Amount | Based on home value and outstanding loan | Based on the course and the institution |

| Moratorium Period | No moratorium (interest accrues immediately) | Typically course period + 6-12 months |

| Processing Fee | May already be set up (no additional fee) | 1-2% of the loan amount |

| Collateral | Home has already been used as collateral | May require collateral for loans >₹7.5 lakhs |

Case Study: How the Sharma Family Saved ₹4.5 Lakhs with Credit Dharma

The Sharma Family’s Financial Journey with Home Loan Overdraft:

Background: The Sharma family from Pune took a home loan of ₹80 lakhs for 20 years at 9.25% interest in 2020. In 2022, they converted to an overdraft facility with SBI MaxGain.

Financial Pattern: Mr. Sharma, a sales professional, receives quarterly bonuses. Mrs. Sharma, a freelance consultant, has irregular income patterns.

Overdraft Usage Strategy:

- The family maintained a minimum balance of ₹5 lakhs in their overdraft account

- Each quarter, they deposited Mr. Sharma’s bonus (averaging ₹2 lakhs)

- They withdrew funds only for significant expenses (home renovation, family wedding)

- Mrs. Sharma’s consulting income was directly deposited into the overdraft account

Five-Year Financial Impact:

- Original Home Loan Interest (projected for 5 years): ₹34.65 lakhs

- Interest Paid with Overdraft Strategy: ₹30.15 lakhs

- Total Interest Saved: ₹4.5 lakhs

- Additional Benefit: Withdrawn ₹12 lakhs for renovation without taking a separate loan

Key Success Factors:

- Disciplined approach to deposits and withdrawals

- Using the overdraft primarily for significant expenses

- Regular monitoring of the account balance

- Automating deposits from income sources

Home Loans With Overdraft Facility: Calculation Examples with Real Numbers

Interest Savings Calculations

Let’s understand the potential interest savings with detailed calculations for a ₹50 lakh home loan at 9% interest for 20 years:

Regular Home Loan:

- EMI: ₹44,986

- Total Interest Paid over 20 years: ₹57,96,640

With Overdraft Facility – Scenario 1 (₹5 lakhs constant deposit):

- Effective loan amount: ₹45 lakhs

- Interest calculated on: ₹45 lakhs

- EMI remains: ₹44,986

- Monthly interest saving: ₹3,750

- Annual interest saving: ₹45,000

- Total interest saving over 20 years: ₹9,00,000

With Overdraft Facility – Scenario 2 (Variable deposits): Let’s assume a more realistic scenario with fluctuating balances:

- Year 1-5: Average balance of ₹3 lakhs

- Year 6-10: Average balance of ₹7 lakhs

- Year 11-15: Average balance of ₹10 lakhs

- Year 16-20: Average balance of ₹5 lakhs

Total interest saving over 20 years with this pattern: Approximately ₹6,25,000

With Overdraft Facility – Scenario 3 (Increasing deposits): Starting with ₹2 lakhs and increasing the deposit by ₹1 lakh every year:

- Total interest saving over 20 years: Approximately ₹10,50,000

Amortization Comparisons

The table below shows a comparison of amortization schedules for a ₹50 lakh loan over the first 5 years:

| Year | Month | Regular Home Loan | With ₹5 Lakhs in Overdraft | ||||

|---|---|---|---|---|---|---|---|

| EMI Payment | Principal Payment | Interest Payment | EMI Payment | Principal Payment | Interest Payment | ||

| 1 | 1 | ₹44,986 | ₹7,153 | ₹37,833 | ₹44,986 | ₹10,903 | ₹34,083 |

| 1 | 6 | ₹44,986 | ₹7,422 | ₹37,564 | ₹44,986 | ₹11,172 | ₹33,814 |

| 1 | 12 | ₹44,986 | ₹7,750 | ₹37,236 | ₹44,986 | ₹11,500 | ₹33,486 |

| 2 | 6 | ₹44,986 | ₹8,252 | ₹36,734 | ₹44,986 | ₹12,002 | ₹32,984 |

| 2 | 12 | ₹44,986 | ₹8,624 | ₹36,362 | ₹44,986 | ₹12,374 | ₹32,612 |

| 3 | 6 | ₹44,986 | ₹9,181 | ₹35,805 | ₹44,986 | ₹12,931 | ₹32,055 |

| 3 | 12 | ₹44,986 | ₹9,592 | ₹35,394 | ₹44,986 | ₹13,342 | ₹31,644 |

| 4 | 6 | ₹44,986 | ₹10,214 | ₹34,772 | ₹44,986 | ₹13,964 | ₹31,022 |

| 4 | 12 | ₹44,986 | ₹10,668 | ₹34,318 | ₹44,986 | ₹14,418 | ₹30,568 |

| 5 | 6 | ₹44,986 | ₹11,361 | ₹33,625 | ₹44,986 | ₹15,111 | ₹29,875 |

| 5 | 12 | ₹44,986 | ₹11,866 | ₹33,120 | ₹44,986 | ₹15,616 | ₹29,370 |

Key Observations:

- With ₹5 lakhs in the overdraft account, more of your EMI goes toward principal repayment

- After 5 years with a regular loan, you’ve paid ₹26.96 lakhs in interest

- After 5 years with ₹5 lakhs in overdraft, you’ve paid ₹24.21 lakhs in interest

- Interest savings after 5 years: ₹2.75 lakhs

Tax Impact Calculations

The tax implications of a home loan overdraft facility can significantly affect your overall financial benefits:

Tax Savings Comparison for a ₹50 Lakh Loan (for a person in a 30% tax bracket):

| Year | Regular Home Loan | With ₹10L in Overdraft | Difference in Tax Benefit | ||

|---|---|---|---|---|---|

| Interest Paid | Tax Saving | Interest Paid | Tax Saving | ||

| 1 | ₹4,45,000 | ₹1,33,500 | ₹3,60,000 | ₹1,08,000 | -₹25,500 |

| 2 | ₹4,35,000 | ₹1,30,500 | ₹3,50,000 | ₹1,05,000 | -₹25,500 |

| 3 | ₹4,24,000 | ₹1,27,200 | ₹3,39,000 | ₹1,01,700 | -₹25,500 |

| 4 | ₹4,12,000 | ₹1,23,600 | ₹3,27,000 | ₹98,100 | -₹25,500 |

| 5 | ₹3,99,000 | ₹1,19,700 | ₹3,14,000 | ₹94,200 | -₹25,500 |

| Total | ₹21,15,000 | ₹6,34,500 | ₹16,90,000 | ₹5,07,000 | -₹1,27,500 |

Interest Savings vs. Tax Benefit Analysis:

- Interest saving with ₹10L in overdraft over 5 years: ₹4,25,000

- Reduction in tax benefits: ₹1,27,500

- Net financial advantage: ₹2,97,500

Important Note: The tax benefit difference should be weighed against the interest savings to determine the true financial benefit of the overdraft facility.

How to Apply for a Home Loan with Overdraft Facility

Step-by-Step Application Process

Follow these steps to apply for a home loan with an overdraft facility:

- Research and Compare Options

- Research banks offering overdraft facilities

- Compare interest rates, fees, and features

- Calculate potential savings based on your financial situation

- Read customer reviews and experiences

- Check Eligibility

- Verify your credit score (aim for 750+)

- Calculate your debt-to-income ratio (should be less than 50%)

- Ensure property meets bank’s criteria

- Check income requirements

- Document Preparation

- Gather identity and address proof documents

- Organize income proof documents

- Compile property documents

- Prepare financial statements

- Loan Application

- Fill the home loan application form

- Specifically request the overdraft facility option

- Submit all required documents

- Pay the application/processing fee

- Property Evaluation

- Bank conducts legal verification of property

- Technical valuation of property conducted

- Evaluation report generated

- Loan Approval and Agreement

- Receive and review loan approval letter

- Verify terms and conditions of the overdraft facility

- Sign loan agreement documents

- Complete mortgage/hypothecation formalities

- Disbursement and Account Setup

- Loan disbursement to seller/builder

- Overdraft account creation

- Receive account details and access methods

- Set up online banking access for the overdraft account

- Post-Disbursement

- Begin EMI payments

- Start utilizing the overdraft facility

- Set up account monitoring systems

- Regularly review account statements

Digital Application Options

Most major banks now offer digital application channels for home loans with overdraft facilities:

Mobile Banking Applications:

- SBI YONO

- ICICI iMobile

- HDFC Bank Mobile Banking

- Axis Mobile

- Citibank Mobile

Online Banking Portals:

- Most banks allow applications through their websites

- Online document upload options

- Video KYC facilities

- Digital signature capabilities

Digital-First Process Benefits:

- 24/7 application submission

- Faster processing times

- Real-time application status tracking

- Digital document submission

- Pre-approved loan offers for existing customers

Typical Digital Application Timeline:

- Online application: 30 minutes

- Document verification: 2-3 days

- Digital property verification: 5-7 days

- Online approval: 1-2 days

- Digital loan agreement: 1 day

- Account setup: 1-2 days

- Total digital process: 10-15 days (compared to 21-35 days for traditional process)

Common Reasons for Rejection

Understanding common rejection reasons can help you prepare a stronger application:

- Low Credit Score

- Home loan overdraft facilities typically require higher credit scores (750+)

- Recent credit defaults or late payments can lead to rejection

- Solution: Work on improving your credit score before applying

- Insufficient Income Documentation

- Irregular income patterns without proper documentation

- Inadequate banking history

- Solution: Maintain detailed financial records for at least 2 years

- Property-Related Issues

- Legal complications with property title

- Property in unauthorized colonies or areas

- Incomplete construction or regulatory approvals

- Solution: Conduct thorough property due diligence before applying

- High Debt-to-Income Ratio

- Existing loan obligations that exceed 50% of income

- Multiple ongoing EMIs

- Solution: Reduce existing debt before applying

- Insufficient Employment Stability

- Frequent job changes in recent years

- Less than 2 years in current organization (for salaried)

- Solution: Apply after achieving employment stability

- Incomplete Documentation

- Missing property documents

- Incomplete income proof

- Inconsistencies in submitted documents

- Solution: Use a document checklist and verify all papers before submission

Recovery Strategy: “If your home loan overdraft application is rejected, request detailed feedback from the bank. Address the specific issues and reapply after 3-6 months. Alternatively, consider applying to a different bank with more suitable eligibility criteria for your situation.” – Mortgage Advisor with 12+ years of experience

Switching to an Overdraft Facility

Home Loan Balance Transfer Basics

If your current lender doesn’t offer an overdraft facility or provides unfavorable terms, you might consider transferring your home loan to a bank that offers better overdraft options:

What is a Home Loan Balance Transfer? A home loan balance transfer involves moving your existing home loan from one lender to another, typically to benefit from lower interest rates, better terms, or additional facilities like overdraft.

Key Components of Balance Transfer:

- Transfer of outstanding loan amount to the new lender

- New loan agreement with the new bank

- Release of property documents from the old lender

- Creation of new mortgage/lien in favor of the new lender

- Setting up of new repayment mechanism

Balance Transfer Process Timeline:

- Application to new bank: 1 day

- Credit assessment and approval: 5-7 days

- Loan offer from new bank: 1-2 days

- Acceptance and documentation: 2-3 days

- NOC request to existing bank: 1 day

- Existing bank processing and NOC issuance: 7-15 days

- Property document transfer: 3-5 days

- New loan disbursement: 2-3 days

- Overdraft account setup: 2-3 days Total timeline: 23-40 days

Costs Involved in Switching

Before deciding to switch, carefully evaluate all associated costs:

Direct Costs:

| Fee Type | Typical Range | Notes |

|---|---|---|

| Processing Fee (New Bank) | 0.5% – 1% of loan amount | Some banks offer discounts during promotional periods |

| Foreclosure Charges (Old Bank) | 0% – 2% of outstanding amount | Many banks have waived foreclosure charges on floating rate loans as per RBI guidelines |

| MOD (Memorandum of Deposit) Charges | ₹500 – ₹2,000 | For creating new mortgage |

| Legal Verification Fee | ₹3,000 – ₹7,000 | For property title verification |

| Technical Valuation Fee | ₹2,500 – ₹5,000 | For property value assessment |

| Stamp Duty | Varies by state (0.1% – 0.5%) | On loan agreement documents |

| Documentation Charges | ₹500 – ₹1,500 | For new loan agreement |

| CERSAI Registration | ₹500 – ₹1,500 | For registering the new mortgage |

Indirect Costs:

- Time invested in research and application process

- Multiple visits to banks and documentation centers

- Temporary impact on credit score due to new loan inquiry

- Transitional interest (interest for days between disbursement and first EMI)

Illustrative Example of Switching Cost: For a ₹50 lakh outstanding loan:

- Processing fee (0.75%): ₹37,500

- Foreclosure charges (assuming 0%): ₹0

- Legal and technical fees: ₹10,000

- Stamp duty (0.2%): ₹10,000

- Other charges: ₹5,000

- Total cost: ₹62,500

Break-even Analysis: If switching to a bank with overdraft facility saves you 0.5% in effective interest:

- Annual saving on ₹50 lakhs: ₹25,000

- Break-even period: Approximately 2.5 years

Timeline and Process

The balance transfer and overdraft conversion process typically follows these stages:

Pre-Application Stage (1-2 weeks):

- Research lenders offering overdraft facilities

- Compare interest rates and terms

- Calculate potential savings and break-even period

- Collect necessary documents

Application Stage (1 week):

- Submit application to new lender

- Property verification and valuation

- Credit assessment

- Receive loan offer letter

Documentation Stage (1-2 weeks):

- Accept offer letter

- Submit required documents

- Sign loan agreement

- Request NOC from existing lender

Transition Stage (1-2 weeks):

- Receive NOC from existing lender

- Transfer of property documents

- Loan disbursement to existing lender

- Closure of old loan

Setup Stage (1 week):

- Overdraft account creation

- Online banking setup

- Standing instruction for EMI

- Receipt of welcome kit

Best Practices for Smooth Transition:

- Begin the process at least 45-60 days before your desired switch date

- Keep digital copies of all documents ready for quick submission

- Maintain EMI payments to your existing lender until confirmation of loan closure

- Obtain a loan closure certificate from your previous lender

- Update your credit bureau records after the transfer is complete

Expert Tip: “The best time to transfer your loan for an overdraft facility is after 3-5 years of your original loan. By this time, you’ve built equity in the property, reduced the principal significantly, and can negotiate better terms with the new lender.” – Senior Housing Finance Professional

Income Tax Benefits of Having a Home Loan Overdraft Account

Section 24 Benefits

Section 24 of the Income Tax Act allows deduction of interest paid on housing loans. Here’s how it applies to overdraft facilities:

Basic Tax Benefit Structure:

- For self-occupied property: Interest deduction up to ₹2 lakhs per financial year

- For let-out property: Entire interest amount is deductible

How Overdraft Affects Section 24 Benefits:

- Interest is calculated only on the net outstanding loan (after considering the balance in the overdraft account)

- Only the actual interest paid is eligible for tax deduction

- Depositing funds in the overdraft account effectively reduces your tax deduction under Section 24

Optimization Strategy: For maximizing both interest savings and tax benefits, consider:

- Maintaining overdraft balance just below the amount that would reduce your interest below ₹2 lakhs (for self-occupied property)

- Timing your deposits to maximize both benefits

- Consulting a tax advisor for personalized optimization

Principal Repayment Benefits

Section 80C of the Income Tax Act provides deduction for principal repayment of home loans:

Basic Benefit Structure:

- Principal repayment eligible for deduction under Section 80C

- Maximum deduction limit of ₹1.5 lakhs per year (combined with other 80C investments)

Impact of Overdraft on Principal Repayment Benefits:

- Principal repayment schedule remains the same regardless of overdraft balance

- Full EMI principal component remains eligible for deduction

- No negative impact on Section 80C benefits from overdraft usage

Tax Planning Opportunity: Since the overdraft facility doesn’t affect your principal repayment deduction, you can:

- Optimize your overdraft usage for interest savings

- Continue claiming full principal repayment under Section 80C

- Use the freed-up cash flow for other tax-saving investments

Documentation for Tax Filing

Proper documentation is crucial for claiming tax benefits on home loans with overdraft facilities:

Essential Documents for Tax Filing:

- Loan Account Statement showing:

- Principal repayment for Section 80C

- Interest paid for Section 24

- Overdraft account transactions

- Interest Certificate issued by the bank annually or on request

- Provisional Interest Certificate if filing returns before receiving annual certificate

- Home Loan Agreement showing loan purpose and property details

- Property Purchase Documents including sale deed and registration documents

- Overdraft Facility Agreement showing the terms of the facility

Special Documentation Requirements:

- Request a separate interest paid certificate specifically mentioning the net interest after considering overdraft balance

- Maintain records of all deposits and withdrawals from the overdraft account

- For joint loans, obtain a certificate showing the individual share of interest paid

Tax Filing Tips:

- File ITR-2 if you have income from house property

- Report the property details in Schedule AL if applicable

- Claim Section 24 deduction in the “Income from House Property” section

- Claim Section 80C deduction for principal repayment in the “Deductions” section

- Attach interest and principal repayment certificates as supporting documents

Tax Planning Insight: “For high net worth individuals in the highest tax bracket, the reduced tax benefit from lower interest payments may partially offset the interest savings. However, the flexibility to withdraw funds without tax implications when needed often outweighs this disadvantage.” – Chartered Accountant specializing in real estate taxation

Managing Your Home Loan Overdraft Effectively

Best Practices for Maximum Benefit

Follow these strategies to maximize the benefits of your home loan overdraft facility:

Financial Management Strategies:

- Maintain a Threshold Balance

- Keep a minimum balance of 3-6 months’ expenses

- Avoid withdrawing below this threshold except for emergencies

- Replenish the threshold amount as soon as possible

- Strategic Deposit Timing

- Deposit funds immediately after receiving income

- Even a few days’ earlier deposit can reduce interest significantly

- Consider restructuring salary credits directly to the overdraft account

- Withdrawal Discipline

- Withdraw only for significant expenses or investments

- Avoid using the overdraft for regular expenses

- Create a withdrawal approval process (for families)

- Surplus Fund Allocation

- Compare potential returns from investments vs. interest savings

- For investments yielding less than loan interest rate, prioritize keeping funds in overdraft

- For higher-yielding investments, consider partial allocation

- Regular Monitoring

- Review account statement monthly

- Track interest savings quarterly

- Re-evaluate strategy annually

Digital Tools for Tracking and Management

Leverage technology to optimize your overdraft facility management:

Mobile Banking Features for Overdraft:

- Real-time balance monitoring

- Automated alerts for large withdrawals

- Scheduled transfers between accounts

- Interest calculation tools

- Transaction categorization

Third-Party Financial Management Apps:

- Money Manager

- Walnut

- ET Money

- Perfios

- Mint

Excel Templates and Calculators: Create or use templates for:

- Interest savings tracking

- Withdrawal impact analysis

- Deposit optimization

- Tax benefit calculations

- Break-even analysis

Digital Banking Features to Enable:

- SMS/Email alerts for all transactions

- Periodic account summary notifications

- Low balance alerts

- Standing instructions for auto-sweeping funds

- Overdraft limit utilization notifications

Common Mistakes to Avoid

Be aware of these pitfalls that can reduce the effectiveness of your home loan overdraft facility:

- Treating Overdraft as Free Money

- The flexibility to withdraw can lead to unnecessary spending

- Solution: Create clear withdrawal criteria and stick to them

- Ignoring Account Maintenance Fees

- Quarterly/annual maintenance fees can add up

- Solution: Include these costs in your overall financial calculations

- Neglecting to Monitor Interest Calculations

- Banks may occasionally make errors in interest calculations

- Solution: Regularly verify interest charges against your balance

- Using Overdraft for Lifestyle Inflation

- Easy access to funds can lead to lifestyle upgrades

- Solution: Distinguish between needs, wants, and investments before withdrawals

- Withdrawing for Low-Return Investments

- Investing in products yielding less than your loan interest rate

- Solution: Compare potential returns against guaranteed interest savings

- Failing to Adjust Strategy with Interest Rate Changes

- Overdraft benefits change as interest rates fluctuate

- Solution: Reassess your strategy with every interest rate change

- Not Coordinating with Joint Holders

- Miscommunication with co-borrowers about deposits/withdrawals

- Solution: Create shared access protocols and decision frameworks

Financial Advisor’s Perspective: “The biggest mistake people make with home loan overdraft facilities is psychological – they feel wealthy seeing a large accessible balance, leading to spending temptations. The most successful users create mental or actual barriers between their ‘accessible’ and ‘untouchable’ portions of the overdraft balance.” – Wealth Management Consultant

Expert Opinions and Market Trends

What Financial Advisors Recommend

Leading financial experts have varying recommendations on home loan overdraft facilities:

For Salaried Professionals:

“Salaried professionals with stable incomes should consider maintaining 30-40% of their annual income in the overdraft account. This provides both interest savings and emergency liquidity.” – Vikram Sharma, Certified Financial Planner

For Business Owners:

“Business owners with cyclical cash flows can leverage the overdraft facility to balance personal and business finances. During peak business seasons, park surplus funds in the overdraft account, and withdraw during lean periods.” – Anjali Kapoor, Business Financial Consultant

For Investors:

“Compare the post-tax returns on potential investments with the interest savings from the overdraft. For most conservative investors, keeping funds in the overdraft account until genuinely profitable investment opportunities arise is the optimal strategy.” – Rajesh Mehta, Investment Advisor

Consensus Recommendations:

- Best suited for individuals with variable income or occasional lump sums

- Most beneficial in the first 7-10 years of the loan when interest component is highest

- Should be combined with proper financial discipline and regular monitoring

- More advantageous for loans with longer remaining tenures

- Should be evaluated annually against other financial products

Future of Home Loan Overdraft in India

The home loan overdraft landscape in India is evolving rapidly:

Current Market Trends:

- Increasing adoption by mid-sized and smaller banks

- Digital-first implementation reducing operational complexities

- More competitive features and lower maintenance charges

- Enhanced integration with overall banking services

- Tailored overdraft products for specific professions (doctors, chartered accountants, etc.)

Regulatory Developments:

- RBI’s continued focus on transparency in banking products

- Potential standardization of overdraft terms across lenders

- Increased consumer protection measures

Future Predictions:

- AI-Powered Optimization: Smart algorithms suggesting optimal deposit and withdrawal patterns

- Integrated Financial Ecosystem: Better connection with investment platforms and financial planning tools

- Flexible Interest Calculation: Daily or even real-time interest calculations versus monthly

- Hybrid Products: Combinations of overdraft facilities with investment components

- Specialized Variations: Industry or profession-specific overdraft products with tailored features

Industry Expert View:

“The future of home loan overdraft in India is heading toward greater personalization and flexibility. We expect to see products that automatically optimize between interest savings and investment returns based on the customer’s financial goals and risk appetite.” – Banking Innovation Head at a leading financial institution

Conclusion

The Overdraft Facility Calculator stands out as a pivotal tool in managing your home loan. By understanding and utilizing this calculator, you’re taking a proactive step towards optimizing your loan repayments and enhancing your financial health. Remember, every bit extra you repay on your loan can significantly reduce the amount of interest you pay over the life of the loan and shorten your loan term.

Making informed decisions about your home loan overdraft facility is crucial to your financial wellbeing. If you’re considering to explore OD options , let Credit Dharma guide you

Frequently Asked Questions

An Overdraft (OD) facility in a home loan is a feature that allows you to deposit extra money into your loan account, beyond your regular mortgage repayments. This reduces the loan balance temporarily, decreasing the interest charged. You can withdraw the extra funds if needed, offering flexibility while potentially saving on interest and shortening the loan term.

Yes, by depositing extra funds into your overdraft account, you reduce the principal amount of your loan more quickly than scheduled. This reduction in the principal balance results in lower interest charges, potentially saving you a significant amount of money over the life of your loan. The actual savings will depend on the amount of extra funds you deposit and how long they remain in the account.

It’s a good idea to use the calculator periodically. Especially if there are significant changes in your financial situation, interest rates. Or if you’re planning to deposit a lump sum into your overdraft account. Regularly reviewing your loan and potential savings can help you stay on track with your financial goals.

Not at all. Most Overdraft Facility Calculators are user-friendly. They require only basic information about your loan, such as the loan amount, interest rate, term, and the amount of extra money you plan to deposit. By inputting this information, the calculator can show you how using the facility could affect your loan term and interest payments.

HDFC Home Loan

HDFC Home Loan SBI Home Loan

SBI Home Loan