Time is precious, especially in the real estate market. Buying a home is exciting—but home loans can feel overwhelming. Credit Dharma is here to change that. From your first click to final approval, our straightforward online process and dedicated support team make applying for a PNB Housing Finance Home Loan smooth, transparent, and stress-free. Start your application online anytime, anywhere—no more waiting in long queues.

PNB Housing Finance Home Loan: Online Application Process

- Visit the PNB Housing Finance official website.

- Navigate to the “Loans Products” tab. From the dropdown menu, select “Home Loan” to begin your application.

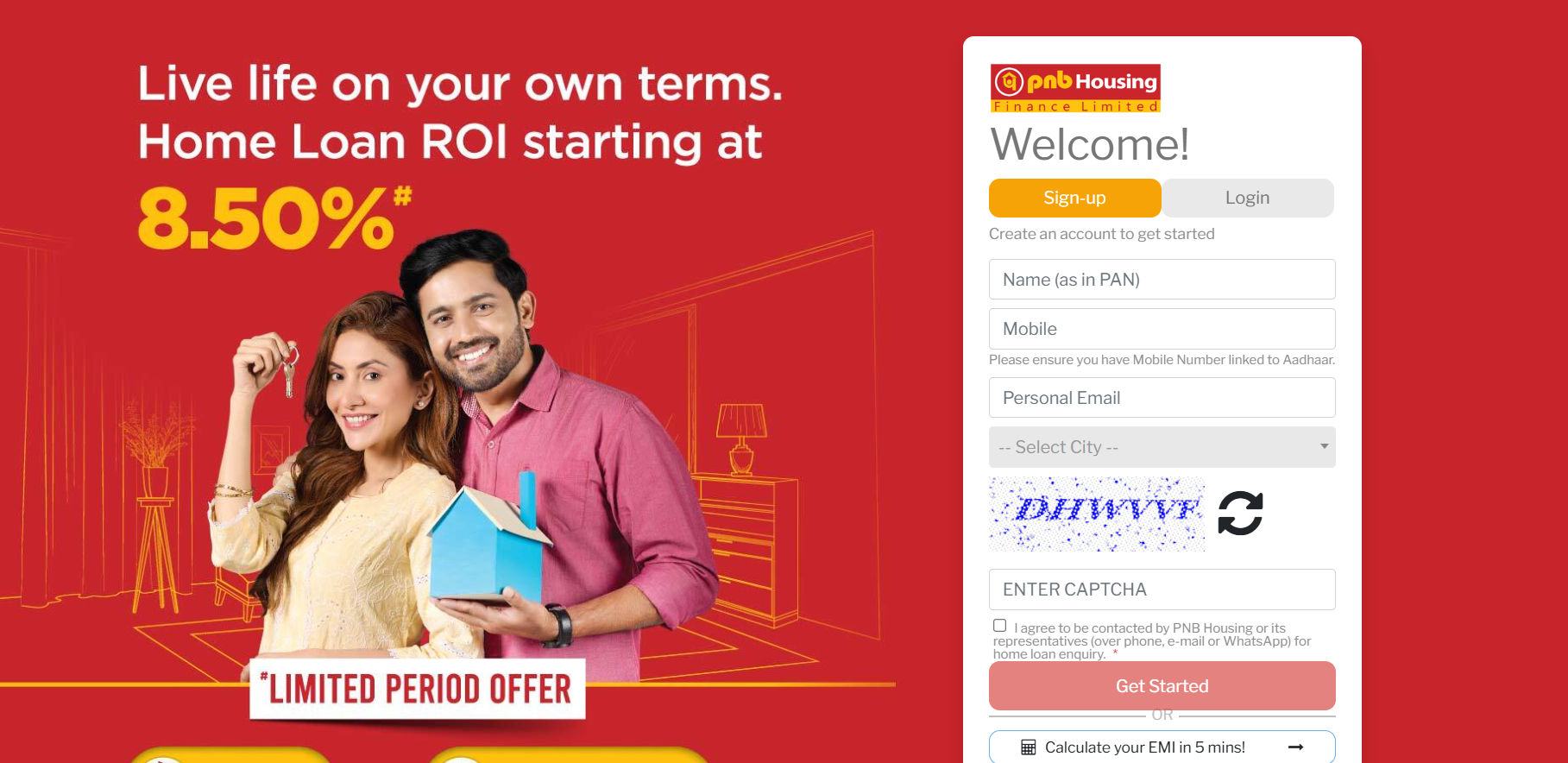

- Scroll down to find the “Apply Now” button.

- Fill in your personal details, including your PAN ID, mobile number, and email address to create an account.

- After registration, you will be redirected to an online application form. Complete all the required fields, including details about your property, income, and employment.

- Submit the necessary documents such as identity proof, address proof, income proof, and property documents, as requested by PNB Housing Finance.

- Review all the entered information and documents. Once everything is correct, click on the “Submit” button to send your application.

- Upon successful submission, you will receive an application reference number for tracking your home loan application.

Suggested Read: PNB Housing Finance Home Loan Interest Rates 2025

PNB Housing Finance Home Loan: Offline Application Process

- Locate Nearest Branch: Visit your nearest PNB Housing Finance branch or authorized representative office.

- Consult Loan Advisor: Discuss loan requirements, eligibility, and interest rates with the loan advisor at the branch.

- Obtain Application Form: Collect the home loan application form from the branch office.

- Fill Application Form: Complete the application form carefully with accurate personal, employment, and property details.

- Gather Required Documents: Attach necessary documents like ID proof, address proof, income proof, bank statements, and property documents.

- Submit Application Form: Hand over the filled application form along with documents at the branch.

Suggested Read: PNB HFC Home Loan Eligibility Criteria

PNB Housing Finance Home Loan Application Process with Credit Dharma

- Visit Credit Dharma’s official website.

- Enter your name, city of residence, and mobile number.

- Choose your preferred loan type, for example “home loan”.

- Enter the OTP and click on “verify.”

- Enter your property details, employment type, income, and CIBIL score.

- Now sit back and relax. Home Loan Experts from Credit Dharma will call you in next 24 Hours.

Suggested Read: PNB Housing Finance Home Loan Documents

PNB Housing Finance Home Loan Application Approval to Disbursement Stages

| Stage | Description |

|---|---|

| Loan Approval Notification | Receive loan approval notification via email/SMS, including approved loan details. |

| Loan Agreement Signing | Visit branch to review and sign loan documents after reading terms carefully. |

| Submission of Original Documents | Submit all required original property documents and sale agreements. |

| Verification of Documents | PNB Housing Finance conducts legal and technical verification of submitted documents. |

| Final Sanction Letter Issuance | Receive formal sanction letter with final loan amount, interest rate, EMI, and loan tenure. |

| Payment of Processing Fees | Pay applicable processing and administrative charges outlined in sanction letter. |

| Request for Loan Disbursement | Submit formal request for disbursement with supporting documents (e.g., builder’s demand letter). |

| Loan Amount Disbursal | PNB Housing Finance disburses loan amount to builder, seller, or as agreed. |

| Loan Repayment Commencement | Begin regular EMI payments as per repayment schedule in your loan agreement. |

Suggested Read: PNB Home Loan Repayment Options

Get a Home Loan

with Highest Eligibility

& Best Rates

How Long Does it Take to Process a Home Loan Application?

| Stage | Key Activities | Estimated Time | Factors Affecting Time |

|---|---|---|---|

| 1. Application Submission | Submit application (online/offline) with documents. | Online: Instant Offline: 1–2 days | Document completeness, submission mode (online vs. offline). |

| 2. Eligibility Check | Credit score assessment, income verification, debt analysis. | 3–5 business days | Credit profile, income stability, existing debts. |

| 3. Property Valuation | Third-party valuation of property’s market value. | 3–7 days | Property type (under-construction/ready), legal clarity. |

| 4. Loan Sanction | Approval of loan amount, interest rate, and terms. | 2–3 days post-valuation | Compliance with LTV ratio, valuation report. |

| 5. Legal & Technical Check | Verify property title, ownership, structural safety, and regulatory approvals. | 5–10 days | Property disputes, regulatory compliance, builder delays. |

| 6. Documentation | Loan agreement signing, mortgage registration, EMI setup. | 1–3 days | Applicant responsiveness, document accuracy. |

| 7. Disbursement | Funds transferred to seller/builder. | 1–3 days (ready property) | Builder coordination, escrow formalities. |

Total Processing Time

- Best Case : 2–3 weeks (ready property, no delays).

- Typical Case : 4–6 weeks (standard processing).

- Under-Construction : 6–8 weeks (phased disbursement).

Suggested Read: How to Track PNB HFC Home Loan Application Status?

Conclusion

Buying a home is a big step. Getting a home loan can be hard, but we make it easy. Choosing Credit Dharma for your home loan simplifies this process. We offer expert advice and personalized assistance to make everything hassle-free. You’ll receive timely updates on your loan application and disbursement progress.

From the initial application to the final disbursement, we provide comprehensive support. Enjoy clear and honest communication at every stage, with no hidden surprises.

Frequently Asked Questions

The maximum loan tenure for a PNB Housing Home Loan is up to 30 years or until the borrower reaches the age of 70 at loan maturity.

To be eligible, applicants must be at least 21 years old, with a minimum monthly income of ₹15,000. A CIBIL score of 611 or above is also required, along with 3+ years of work experience or business continuity.

For salaried individuals, documents include a completed loan application form, identity and address proof, last 3 months’ salary slips, Form 16, 6 months’ bank statements, and property-related documents. Self-employed individuals will need business income proof, tax returns, balance sheets, and business bank statements.

Applicants can apply for a PNB Home Loan online through the official PNB website or via the PNB ONE mobile app. The process involves filling out an application form and uploading the necessary documents.

Applicants can track their home loan application status through the official PNB website, the PNB ONE mobile app, or by visiting the nearest PNB branch.

HDFC Home Loan

HDFC Home Loan SBI Home Loan

SBI Home Loan